The entity known as CoreWeave – a designation that feels less a name than a bureaucratic inventory number – recently divulged its accounts for the final quarter of the last year. The pronouncements, predictably, failed to elicit enthusiasm from those who traffic in these ephemeral valuations. A decline, a yielding of sixty percent from the illusory peak reached in the prior summer, followed. It is a familiar pattern: the ascent built on sand, the inevitable subsidence.

This CoreWeave, sprung forth from the initial public offering not long ago, has enjoyed a period of accelerated growth. Yet, beneath the surface of these reported gains lurks a disquieting imbalance. Capital expenditure, a relentless outward flow of resources, and the specter of an artificial intelligence ‘bubble’ – a term freighted with the memory of past enthusiasms and subsequent collapses – have cast a pall over its prospects. The predictable consequence was a ‘panic button’ response, a flinching from the reality of unsustainable expansion.

Savvy observers, those who retain a vestige of skepticism amidst the prevailing fervor, may ponder whether this moment presents an opportunity. Let us, then, examine the particulars, dissect the accounts, and attempt to discern whether this downturn is merely a correction, or a premonition of something more profound.

The Illusion of Progress and the Weight of Expenditure

The reported revenue for the past year registered an increase of one hundred and sixty-eight percent, reaching five point one billion units of currency. However, this apparent prosperity is shadowed by a capital expenditure of fourteen point nine billion. In the final quarter alone, eight point two billion was disbursed – a surge of two hundred and forty-two percent from the prior year. The result? An adjusted net loss, swollen nearly tenfold to six hundred and six million. A prodigious consumption, a gaping maw demanding to be fed.

Yet, this aggressive spending, we are told, is a ‘necessity.’ The demand for computational capacity dedicated to these ‘artificial intelligences’ is purportedly escalating at an astonishing pace, outpacing the available supply. According to the pronouncements of Goldman Sachs – an institution not known for its disinterested observation – a shortfall of nine gigawatts is anticipated in the coming year, growing to ten gigawatts in the years thereafter. A manufactured scarcity, perhaps, designed to justify ever-increasing investment.

CoreWeave has cultivated a clientele of ‘hyperscalers’ and AI companies – entities engaged in the relentless pursuit of computational dominance. At year’s end, a revenue backlog of sixty-seven billion was reported, a fourfold increase from the prior year. A promise of future revenue, contingent upon the fulfillment of obligations, and the continued viability of these demanding patrons.

The company commits itself to fulfilling forty-two percent of this backlog – twenty-eight billion – in the coming years. Thus, the imperative to expand data center capacity, to consume ever-greater quantities of resources. As the Chief Executive Officer explained in the latest earnings pronouncements – a carefully constructed narrative – the company deployed infrastructure ‘faster than expected,’ and brought ‘more capacity online’ than ever before. A testament to efficiency, or a demonstration of relentless, unyielding expenditure?

The company plans to spend thirty to thirty-five billion in capital expenditure in the coming year – a sum significantly exceeding the anticipated revenue of twelve to thirteen billion. Yet, the company expresses ‘confidence’ that these investments will ultimately yield ‘stronger revenue growth.’ A faith-based projection, divorced from the realities of diminishing returns.

CoreWeave anticipates an annualized run rate revenue of seventeen to nineteen billion by year’s end. A calculation based on the revenue generated in the final month, multiplied by twelve. Even more ambitiously, the company projects exceeding thirty billion in annualized run rate revenue by the following year. A projection that strains credulity, and relies on the continuation of an unsustainable trajectory.

Thus, we are invited to anticipate a sixfold increase in revenue by the year 2028. Furthermore, the company estimates that its long-term adjusted operating margin could reach twenty-five to thirty percent – a substantial improvement from the previous year’s reading of thirteen percent. At the same time, CoreWeave professes a commitment to lowering its average cost of capital. A laudable goal, achieved through the reduction of interest rates and the cultivation of broader participation in financing facilities. A complex accounting maneuver, designed to obscure the underlying vulnerabilities.

A Calculation of Risk and the Allure of Speculation

CoreWeave remains unprofitable, and therefore lacks a traditional price-to-earnings ratio. However, its sales multiple of six point six is lower than the average sales multiple of eight point three for the U.S. technology sector. A superficial comparison, designed to mask the underlying deficiencies.

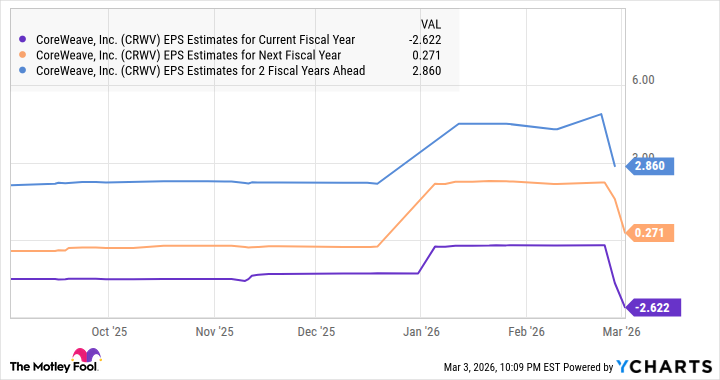

The stock, it is argued, deserves a higher multiple, given its rapid revenue growth. Yet, investors remain preoccupied with bottom-line performance. Fortunately, CoreWeave is ‘likely’ to deliver on that front, as evidenced by the aforementioned chart. Assuming the company achieves earnings of two point eight six per share by 2028, and trades at thirty-two times earnings – in line with the Nasdaq-100 index – its stock could reach ninety-one. A potential increase of twenty-three percent from current levels. A modest gain, contingent upon the fulfillment of ambitious projections.

However, one should not be surprised if even greater gains are realized, given the company’s focus on converting its massive backlog into revenue. A speculative proposition, built on a foundation of debt and unsustainable expansion. The cloud, it seems, is not a realm of ethereal liberation, but a gilded cage, constructed from silicon and fueled by relentless consumption.

Read More

- Gold Rate Forecast

- Silver Rate Forecast

- DOT PREDICTION. DOT cryptocurrency

- Securing the Agent Ecosystem: Detecting Malicious Workflow Patterns

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- NEAR PREDICTION. NEAR cryptocurrency

- EUR UAH PREDICTION

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- Top 15 Insanely Popular Android Games

- USD COP PREDICTION

2026-03-07 19:33