For seventeen years, the market has ascended, a seemingly inexorable climb punctuated only by brief tremors. The convulsion of 2020, a fleeting panic, and the lesser bear of 2022 offered but temporary respite. The Dow Jones, the S&P 500, the Nasdaq – these indices have, for the most part, traced a path ever upward, a testament, some would say, to human ingenuity, though a more cynical observer might suggest merely a prolonged indulgence in hope. Investors, ever susceptible to the siren song of progress, have found solace in the promises of artificial intelligence, the distant allure of quantum computing, and the ever-present balm of corporate share buybacks. The Federal Reserve, too, has played its part, easing the flow of capital and fostering an atmosphere of unwarranted optimism. Yet, such periods of prolonged ascent are rarely, if ever, sustained indefinitely. The weight of expectation, the inevitable accumulation of fragility, and the inherent unpredictability of human affairs conspire to bring all things to a reckoning.

And now, a change approaches. In two months, the very institution that has, for so long, underwritten this expansion may become the instrument of its undoing. The nomination of a successor to the current Chairman, a man of established, if not entirely predictable, temperament, carries with it the potential to disrupt the delicate equilibrium that has sustained this prolonged bull market. It is a truth universally acknowledged that investors abhor uncertainty, yet uncertainty is the very essence of the market itself. The illusion of control, the belief in the possibility of foresight, are comforting fictions, but fictions nonetheless.

The Unintended Consequences of a Nominee

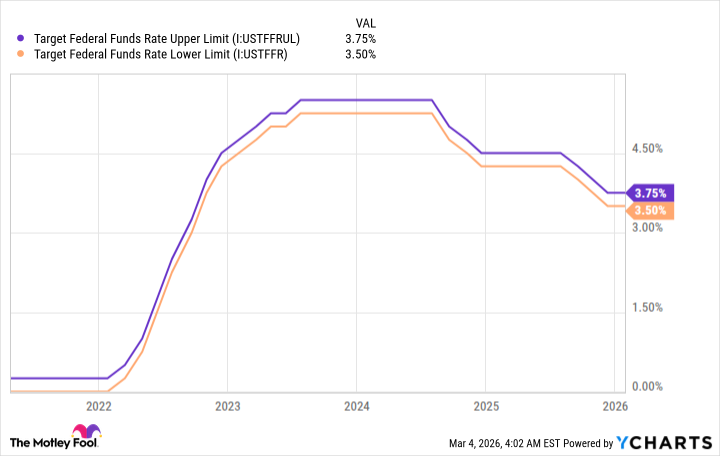

The outgoing Chairman’s term draws to a close, and with it, an era of relative predictability. The incoming nominee, a former Governor and member of the Federal Open Market Committee, is a man of established views, a hawk, as they say, inclined towards restraint and wary of the perils of inflation. This inclination, while perhaps laudable in principle, may prove ill-suited to the current climate, a climate characterized by fragile growth and persistent anxieties. The President, a man not unfamiliar with voicing his displeasure, has made his views known, and the nominee, aware of the source of his appointment, is likely to be receptive to those views. But to govern by decree, to subordinate the dictates of economic prudence to the whims of political expediency, is a dangerous game indeed.

The nominee’s past record reveals a skepticism towards the expansion of the Federal Reserve’s balance sheet, a balance sheet swollen by years of quantitative easing. He views the central bank not as an active participant in the market, but as a detached observer, a custodian of monetary stability. His desire to reduce the balance sheet, to unwind the years of accumulated debt, is understandable in theory, but its practical implications are fraught with peril. For to reduce the supply of money is to raise the cost of borrowing, to stifle investment, and to dampen economic growth. It is a course of action that, while perhaps necessary in the long run, may prove disastrous in the short term.

A Division Within the Ranks

But the nomination itself is not the sole source of concern. A more insidious threat lies within the Federal Open Market Committee itself. For in recent months, a growing fissure has emerged, a divergence of opinion that threatens to undermine the very credibility of the institution. The Committee, charged with the weighty responsibility of guiding the nation’s monetary policy, has been increasingly plagued by dissent, by members who disagree on the proper course of action. This lack of consensus, while perhaps inevitable in a complex and uncertain world, is nonetheless deeply troubling. For investors require a clear and consistent signal, a unified message that inspires confidence and encourages investment. When that signal is obscured by internal strife, when the Committee speaks with multiple voices, the market grows restless and the seeds of doubt are sown.

In the past, a unanimous vote was the norm, a testament to the Committee’s ability to forge a consensus. But in recent months, dissent has become increasingly common, with members voting in opposite directions, each advocating for a different course of action. This lack of unity is a symptom of a deeper malaise, a reflection of the growing complexity of the economic landscape and the difficulty of formulating a coherent policy response. The incoming nominee, a man of strong convictions, is unlikely to bridge this divide. Indeed, he may well exacerbate it, further polarizing the Committee and undermining its credibility.

The market, ever sensitive to shifts in sentiment, will not tolerate such disarray for long. If the Federal Reserve cannot speak with a unified voice, if it cannot provide a clear and consistent signal, the consequences will be severe. The historically high valuations that currently prevail will come under pressure, and the bull market, after its prolonged ascent, will finally succumb to gravity. It is a harsh truth, but a truth nonetheless: the seeds of the next bear market are being sown within the very halls of the Federal Reserve.

Read More

- Gold Rate Forecast

- Securing the Agent Ecosystem: Detecting Malicious Workflow Patterns

- Silver Rate Forecast

- DOT PREDICTION. DOT cryptocurrency

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- EUR UAH PREDICTION

- NEAR PREDICTION. NEAR cryptocurrency

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- USD COP PREDICTION

2026-03-07 14:42