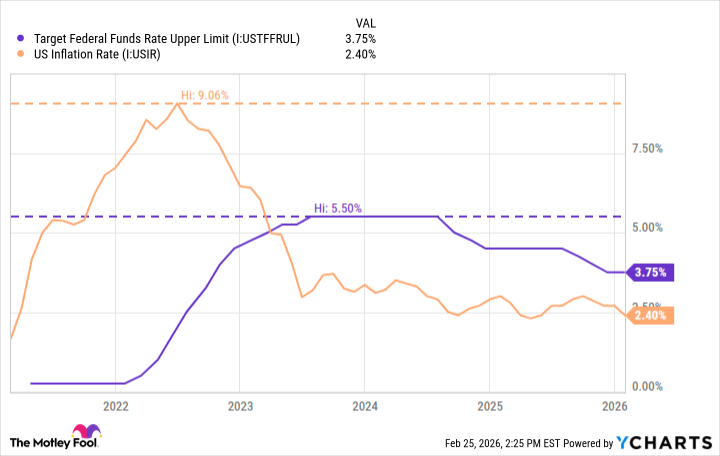

Okay, let’s talk about the Federal Reserve. Because honestly, trying to predict what they’re going to do with interest rates is like trying to assemble IKEA furniture with only a spork. It can be done, but you’re going to need a lot of patience and possibly a therapist. Remember when the S&P 500 was basically rocketing during the Trump years? Good times. Then came the pandemic, stimulus checks, supply chain issues, and suddenly, everything was…less good. Inflation decided to throw a party, and the Fed responded by hiking rates like it was going out of style. Eleven times! That’s a lot of hiking. My Fitbit gets winded after that many steps.

Now, things have cooled off a bit. Inflation is inching closer to the Fed’s 2% target, which, let’s be real, is a completely arbitrary number someone decided sounded good. But here’s the question: will they cut rates this year? It’s a bit like asking if your boss will give you a raise. Technically possible, but you’re probably better off buying lottery tickets.

Are Lower Rates Actually Good for Us? (Besides Making Our Brokers Happy)

The Fed did three little rate cuts last year—each one a quarter of a percent. It’s like getting a 25-cent discount on a $100 bill. Feels good, but doesn’t exactly change your life. The idea is that lower rates make borrowing cheaper, which means people spend more money. More spending equals a healthier economy. It’s a beautiful theory. Except, what if people just use the extra cash to buy avocado toast and vintage vinyl? Then we’re back where we started.

The FOMC—that’s the Federal Open Market Committee, the folks who actually make these decisions—are constantly arguing about this. They’re worried about reigniting inflation. It’s a delicate balancing act. It’s like trying to juggle chainsaws while riding a unicycle. And frankly, I’m starting to suspect they just flip a coin.

Inflation, Interest Rates, and the Ghosts of Economic Missteps Past

The 1970s were…a vibe. Inflation was high, interest rates were all over the place, and everyone was wearing bell bottoms. The Fed cut rates too soon, and inflation came roaring back. It was a lesson learned, apparently. Now, they’re obsessed with hitting that 2% target and keeping real interest rates positive. Which, let’s be honest, is a lot of accounting jargon designed to make us feel like they know what they’re doing.

So, What’s Going to Happen in 2026? (Don’t Ask Me, I Just Write the Jokes)

A few things are at play. First, history. The Fed remembers the 70s, and they’re not eager to repeat those mistakes. Second, inflation is still a little higher than they’d like. And third, the unemployment rate is…well, it’s not terrible, but it’s not exactly stellar either. The Fed has to weigh all these factors, and honestly, it’s exhausting just thinking about it.

But here’s the biggest wildcard: Jerome Powell is leaving in May. Whoever replaces him will have a completely different perspective. It’s like switching directors halfway through a movie. The plot stays the same, but the tone can change drastically. And frankly, that’s the most unpredictable part of the whole equation. New leadership isn’t going to suddenly have access to better data. They’ll just interpret the existing data differently. Maybe they’re an optimist. Maybe they’re a pessimist. Maybe they just really like avocado toast.

My honest take? It’s a coin toss. A genuine, 50/50, flip-a-coin situation. I wouldn’t be shocked if rates go down. I wouldn’t be shocked if they stay the same. What I would be surprised by is if they go up. And honestly, I’m leaning towards no changes at all. The Fed might just decide to sit on the sidelines and watch the chaos unfold. Which, let’s be real, is a perfectly reasonable strategy.

Read More

- Gold Rate Forecast

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- EUR UAH PREDICTION

- DOT PREDICTION. DOT cryptocurrency

- Silver Rate Forecast

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- Core Scientific’s Merger Meltdown: A Gogolian Tale

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

2026-03-04 19:34