![]()

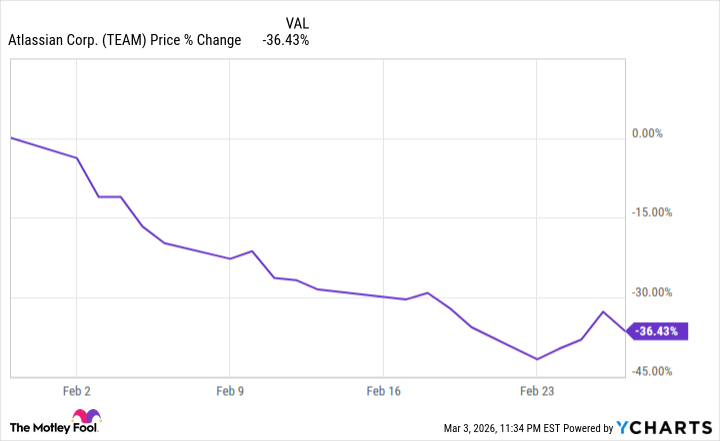

The share price of Atlassian – a name once whispered with the promise of collaborative efficiency – has undergone a marked attenuation. Last month witnessed a decline of thirty-six percent, a grim testament to the prevailing anxieties that grip the software sector. This is not merely a fluctuation of market sentiment, but a slow erosion, a bearing-down of forces that demand scrutiny. The company, purveyor of tools for project management and team cohesion, now finds itself subject to the very pressures it seeks to alleviate in others.

The whispers concern the advent of artificial intelligence. A new order threatens to render obsolete the carefully constructed frameworks of kanban boards and task assignments. The ease with which these emergent intelligences offer customizable solutions – a siren song of simplified organization – has unsettled the market. It is a familiar tale: innovation, rather than building upon the foundations of the past, seeks to dismantle them entirely, leaving in its wake a wreckage of obsolescence.

Atlassian’s clientele – predominantly small and medium-sized enterprises – are particularly vulnerable to this disruptive tide. These businesses, lacking the robust defenses of larger corporations, are exposed to the full force of competitive pressures. They are the first to feel the chill wind of change, the first to bear the brunt of market instability. It is a harsh lesson in the asymmetries of power, the unequal distribution of resilience.

The decline has been protracted, a gradual yielding to forces beyond its immediate control. The chart, a stark visual record of this descent, reveals a steady erosion throughout February, punctuated only by a fleeting, almost illusory, recovery toward the month’s end. It is a pattern reminiscent of a prolonged illness, a slow weakening of vital signs.

The Unfolding of Troubles

Like so many of its peers in the software domain, Atlassian succumbed to a compression of valuation last month, fueled by anxieties surrounding the disruptive potential of artificial intelligence. But there is a particular vulnerability here, a fragility stemming from its focus on smaller enterprises and, more troubling, the absence of consistent, demonstrable profits as measured by generally accepted accounting principles. A structure built on shifting sands, one might say.

The recent earnings report, while superficially positive – revenue increasing by twenty-three percent to $1.59 billion, exceeding estimates – failed to arrest the decline. Adjusted earnings per share also surpassed expectations, rising from $0.96 to $1.22. Yet these figures mask a deeper malaise. The company remains profoundly unprofitable on a GAAP basis, registering an operating loss of $47.7 million for the quarter. A curious accounting, indeed.

The adjusted profits, inflated by a staggering $452.6 million in share-based compensation – exceeding a third of its revenue – are a deceptive mirage. This dilution of shareholder value, while partially offset by stock repurchases, is a subtle erosion of ownership, a transfer of wealth from the many to the few. The repurchases, while commendable, do not address the fundamental imbalance. They are a palliative, not a cure.

This reliance on accounting maneuvers, this skillful manipulation of figures, raises questions about the true health of the enterprise. It is a practice not uncommon in the modern marketplace, but it demands a discerning eye, a refusal to accept appearances at face value. One must look beyond the glossy reports, beyond the carefully crafted narratives, to discern the underlying reality.

The Prospects for Redemption

Atlassian projects full-year revenue growth of twenty-two percent and intends to accelerate share buybacks, a gesture seemingly aimed at bolstering the stock price, which remains down eighty percent from its pandemic-era peak. But these are merely tactical maneuvers, attempts to shore up a weakening position. The fundamental challenge – the threat posed by artificial intelligence and the lack of consistent profitability – remains unaddressed.

The company may need to undertake more drastic measures, to rein in expenses and streamline operations. This could involve difficult choices, perhaps even layoffs. Such a move, while painful, could signal a commitment to fiscal responsibility and a willingness to confront the challenges ahead. It would be a demonstration of resolve, a signal to the market that management is taking the AI threat seriously.

The path forward is fraught with uncertainty. But one thing is clear: Atlassian must demonstrate a commitment to sustainable profitability and a willingness to adapt to the changing landscape. It must shed the illusion of growth and embrace the realities of a competitive marketplace. Only then can it hope to regain the trust of investors and secure its future.

Read More

- Gold Rate Forecast

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- Silver Rate Forecast

- EUR UAH PREDICTION

- DOT PREDICTION. DOT cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

- Core Scientific’s Merger Meltdown: A Gogolian Tale

2026-03-04 08:52