The pronouncements of those who accumulate great wealth are often treated as oracles, their movements parsed for meaning as if the very fate of commerce hinged upon their whims. And so it is with Daniel Loeb, a man whose name echoes through the halls of finance, a manager of considerable fortunes, and a participant in the grand, often merciless, game of capital. Recent filings—those dry, legalistic documents that reveal a glimpse behind the curtain—indicate a shifting of allegiances, a re-evaluation of prospects. He has lessened his holdings in the established behemoths, Amazon and Microsoft, companies that once seemed unassailable, and turned his gaze toward a newer star, a name whispered with increasing reverence: Nvidia.

To sell, of course, is not merely a transaction; it is a judgment. Loeb did not abandon ship entirely, but pruned his stakes—a reduction of twenty-three percent in Amazon, sixteen percent in Microsoft. Such actions are rarely born of simple calculation, but rather a complex interplay of ambition, apprehension, and the ever-present search for advantage. One does not casually relinquish a portion of such holdings without a reasoned expectation of greater returns elsewhere. The market, after all, is not a benevolent provider, but a stern taskmaster, rewarding foresight and punishing complacency.

Nvidia, then, has captured his attention. A company born of the digital age, it has risen with astonishing speed, its fortunes inextricably linked to the burgeoning realm of artificial intelligence. The stock has ascended—a gain of over twelve hundred percent since the year 2023—a testament to both its ingenuity and the boundless optimism surrounding this transformative technology. But such rapid ascent invites scrutiny. Is this a genuine revolution, a harbinger of progress, or merely a speculative bubble, destined to burst under the weight of its own exuberance?

The Persistence of Value

Loeb’s reduced stakes in Amazon and Microsoft should not be interpreted as a condemnation of these companies. They remain formidable forces, their influence woven into the very fabric of modern life. Amazon, the relentless purveyor of goods, has mastered the art of satisfying desire, while Microsoft, the architect of operating systems, continues to shape the digital landscape. Yet even empires must adapt. The pace of innovation is relentless, and those who fail to evolve risk obsolescence. The current year, 2026, has proven unkind to both, a slight cooling after years of uninterrupted growth. This presents a question for those of us who observe these movements: are these temporary setbacks, opportunities to acquire value, or the first signs of a more profound decline?

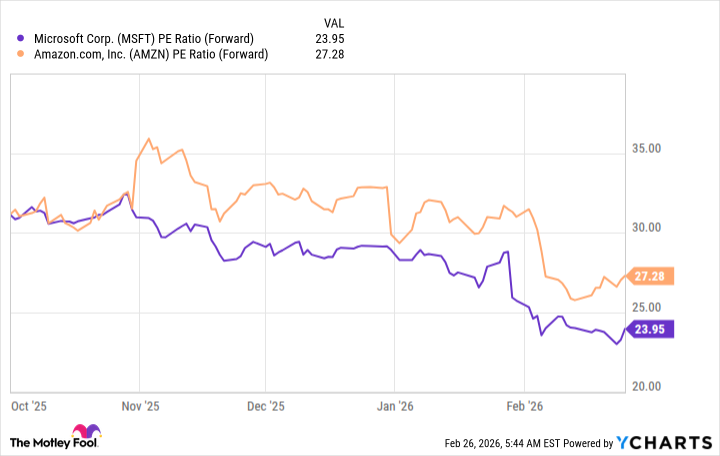

Microsoft, it seems, possesses the more compelling case. Its recent performance—a seventeen percent increase in year-over-year revenue—is a testament to its enduring strength. Furthermore, its cloud computing division flourishes, a vast and ever-expanding realm of possibilities. Amazon, too, has shown resilience, its cloud division enjoying a period of renewed vigor. However, when measured by the cold calculus of forward earnings, Microsoft appears the more reasonably priced of the two. It is a subtle distinction, but one that often separates the prudent investor from the reckless speculator.

One must not dismiss the allure of Nvidia, however. It is a company operating at the very forefront of technological advancement. Its graphics processing units—those intricate silicon hearts—have become indispensable to the development of artificial intelligence. Demand for these processors is insatiable, fueling a period of unprecedented growth. The hyperscalers—those vast data centers that power the digital world—have committed to spending hundreds of billions of dollars on infrastructure, and Nvidia is poised to capture a substantial share of that investment.

The Weight of Expectation

The recent quarterly results—revenue of sixty-eight billion dollars, a seventy-three percent increase year-over-year—are nothing short of remarkable. Nvidia not only met expectations but exceeded them, a testament to its operational prowess and the relentless demand for its products. Yet, even amidst such success, one cannot help but wonder if the market has already priced in all the good news.

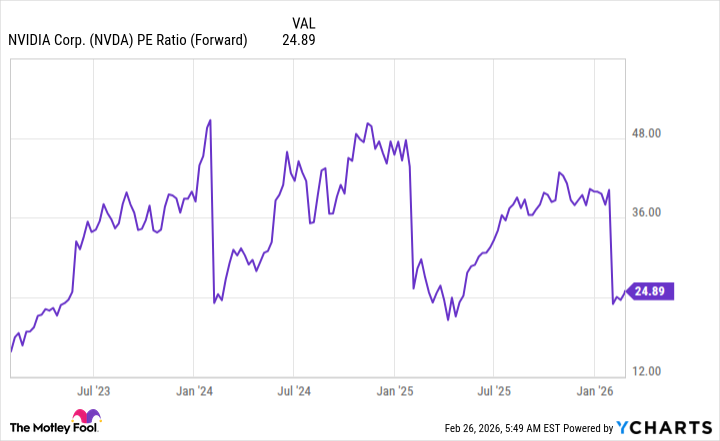

Trading at twenty-five times expected forward earnings, Nvidia appears, surprisingly, to be reasonably valued. Indeed, it is approaching the lowest valuation it has seen in the past three years. This suggests that the market, while acknowledging Nvidia’s potential, remains cautious, wary of the inherent risks associated with such rapid growth.

Thus, one might conclude, with a degree of confidence, that Nvidia remains a compelling investment, a worthy successor to the established giants. To follow in Loeb’s footsteps, to acquire shares of this innovative company, would not be an act of reckless speculation, but rather a calculated bet on the future. And yet, even as we embrace the promise of technological progress, we must never lose sight of the human cost, the ethical dilemmas, and the profound uncertainties that lie ahead. For the pursuit of wealth, like any grand endeavor, is fraught with both opportunity and peril.

Read More

- Gold Rate Forecast

- Top 15 Insanely Popular Android Games

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- EUR UAH PREDICTION

- Silver Rate Forecast

- DOT PREDICTION. DOT cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

- Core Scientific’s Merger Meltdown: A Gogolian Tale

2026-03-04 01:24