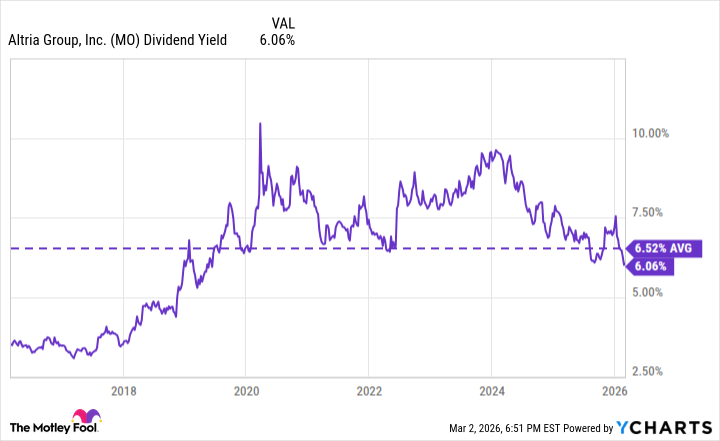

Altria (MO 0.76%), a name that clings to the tongue like a particularly stubborn memory, currently offers a dividend yield of 6.1%. A figure, one might observe, that is not merely generous, but almost…flaunts itself. It surpasses the S&P 500’s modest offering—a mere 1.1%—by a margin that feels, dare I say, theatrical. For a ten-thousand-dollar investment, this translates to an additional five hundred dollars in annual dividend income. A sum sufficient, perhaps, for a weekend devoted to the pursuit of exquisitely rare lepidoptera, or, less poetically, a down payment on a rather dull appliance.

Yet, a yield so…emphatic… invariably prompts a discreet inquiry. Is this a genuine opportunity, a sun-dappled haven for the discerning investor, or merely a gilded cage concealing a more precarious reality? The market, after all, possesses a peculiar fondness for illusions, and often rewards those who skillfully craft them.

The Illusion of Normality

It is, perhaps, surprising to discover that Altria’s current yield, while appearing quite robust, is, in fact, rather low when viewed through the lens of the past decade. There were times—fleeting, yet memorable—when the yield ventured well beyond the 7% mark, even flirting with double digits. The share price, of course, is a capricious mistress, capable of altering the landscape of yields with a mere whim. Nevertheless, Altria has, for the most part, maintained a reputation as a reliably high-yielding concern.

The company’s decades-long history of dividend increases is, admittedly, a compelling narrative. It offers investors a comforting sense of continuity, a promise of future rewards. And Altria anticipates continued, albeit modest, single-digit dividend growth in the years to come. A predictable, if uninspired, trajectory.

The Shadow of Risk

Despite the reliability of Altria’s dividend, I confess to a certain reluctance to recommend this particular investment. The risks, though often obscured by the allure of a high yield, are undeniably present. Tobacco consumption has been in decline for years, a slow but inexorable erosion of the company’s core market. The question of future growth, therefore, hangs heavy in the air, a persistent, unsettling dissonance. While the dividend may appear sustainable today, its long-term viability is, shall we say, open to debate. Last year, the company generated $20.1 billion in revenue, net of excise taxes—a decline of approximately 2% from the previous year. Growth, it seems, is proving to be a particularly elusive quarry.

There exists, naturally, a plethora of other high-yielding dividend stocks, and Altria, in my estimation, simply does not warrant the inherent risk. Its payout ratio hovers around 100%, leaving little margin for error. Should the company require additional capital for growth initiatives, the dividend may, alas, become a necessary casualty. A rather ignominious fate for such a long-standing tradition.

Over the past decade, Altria’s total returns—inclusive of dividends—have amounted to approximately 120%. A respectable figure, perhaps, but woefully inadequate when compared to the S&P 500’s gains of over 310% during the same period. If one seeks truly substantial returns, focusing solely on the dividend may prove to be a rather myopic strategy.

Read More

- Top 15 Insanely Popular Android Games

- Gold Rate Forecast

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- EUR UAH PREDICTION

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- Silver Rate Forecast

- DOT PREDICTION. DOT cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- Core Scientific’s Merger Meltdown: A Gogolian Tale

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

2026-03-03 18:03