Broadcom, you see, isn’t one of those flashy tech companies that hog all the limelight. It’s more the quietly competent sort, the Jeeves of the silicon world, if you will. But don’t let its lack of swagger fool you; it’s absolutely vital to the whole technological shebang, a key player in this modern marvel of artificial intelligence, and a rather dashing one at that. It’s the sort of company that doesn’t shout about its achievements; it simply gets on with being extraordinarily successful.

Shareholders, naturally, have been reaping the benefits of this admirable efficiency. The stock, over the last three years, has performed a positively dizzying jig, climbing a remarkable 437%. A most agreeable sight, wouldn’t you agree? And even in the last twelve months, it’s put on a respectable 60%, which is enough to make even the most hardened City gent crack a smile.

Now, the company faces a bit of a moment of truth on March 4th, when it unveils its latest financial report. The question is, should one, with a perfectly straight face, venture to acquire some shares before the announcement? A tricky business, investing, but let’s have a look at the evidence, shall we? It’s a matter of discerning whether this particular thoroughbred is still capable of a decent gallop.

Chip Shot

Broadcom, you see, isn’t merely a manufacturer of bits and bobs. It’s a purveyor of technological solutions, reaching into every nook and cranny of the industry. Software, semiconductors, security – the whole kit and caboodle. It serves the mobile crowd, the broadband enthusiasts, the cable aficionados, and, most importantly, those chaps running the data centers. A remarkably versatile fellow, Broadcom, wouldn’t you say?

The arrival of AI in early 2023 presented a golden opportunity, and Broadcom, with a commendable display of foresight, positioned itself to profit handsomely. Its Application-Specific Integrated Circuits – rather a mouthful, those – can be tailored to accelerate AI workloads while consuming less energy than those flashy graphics processing units. And it also supplies the networking solutions that form the very backbone of data center operations. A dashedly clever bit of engineering, what!

The results, as one might expect, have been most gratifying. In its last financial quarter, Broadcom generated a revenue of $18 billion – a tidy sum, indeed – up 18% year over year. And its earnings per share jumped a respectable 37%. AI semiconductors led the charge, growing a positively exuberant 74%.

Management, with a characteristic air of optimism, predicts that the good times will continue. For the first quarter, they’re forecasting revenue of $19.1 billion – a 28% increase – and adjusted EBITDA of around $12.8 billion, up 27%. Not bad, not bad at all.

And the dividend? The icing on the cake, as they say. A generous $0.65 per quarter, currently yielding around 0.8%. The stock price, naturally, is soaring, but with a payout ratio of 50% and rising profits, Broadcom seems to have plenty of resources to continue its 15-year streak of dividend increases. A most dependable sort of company, wouldn’t you agree?

Should You Buy Broadcom Stock Before Thursday?

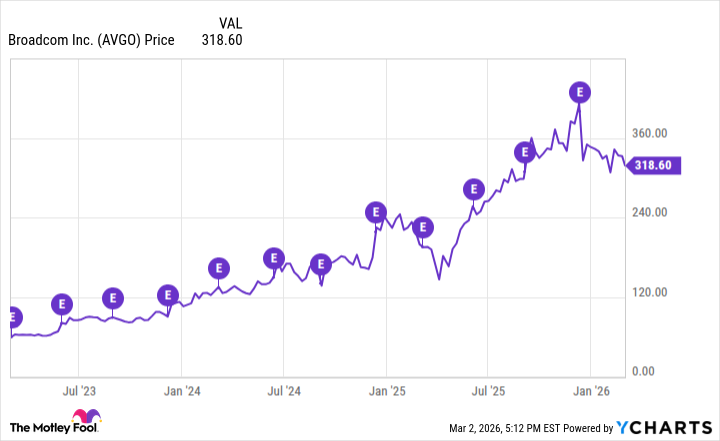

The chart above illustrates Broadcom’s stock price movements over the past three years. The purple circles, marked with a cheerful “E”, indicate the dates of its financial reports. In the majority of cases – a commendable 67% – the stock price has increased after the announcement, as investors, with a perfectly reasonable degree of enthusiasm, piled into the stock.

Broadcom has a habit of underpromising and overdelivering, reporting results that are better than expected and raising its forecasts. Even when investors are initially pessimistic, the company’s long track record of growth and stellar performance eventually wins them over. A most persuasive fellow, Broadcom, wouldn’t you say?

I don’t generally recommend date-driven buying, but instead suggest focusing on the long-term opportunity. For investors looking to establish a position or increase an existing one, now might be a good time. Despite its robust results, Broadcom stock is down 23% from its peak, as investors pause to assess the ongoing adoption of AI. A temporary wobble, I suspect.

What Does Wall Street Have to Say?

Wall Street, it seems, is overwhelmingly bullish. Of the 50 analysts who’ve offered an opinion, a remarkable 96% rate the stock a buy or strong buy. And not a single one recommends selling. A most emphatic endorsement, wouldn’t you agree?

The stock’s valuation might be a sticking point for some investors, as Broadcom is currently selling for 31 times forward earnings. While that might seem a bit pricey, I’d submit it’s a fair price to pay for a company with Broadcom’s track record of success. A bit of a splurge, perhaps, but a worthwhile one.

While investors pause to assess the future of AI, most experts agree that the opportunity continues to unfold. PricewaterhouseCoopers estimates that AI will contribute a staggering $15.7 trillion to the global economy by the end of the decade. A most impressive sum, wouldn’t you say?

Given the company’s successful track record, rising sales and profits, and strong secular tailwinds, the evidence suggests that Broadcom stock is a buy. A perfectly sensible investment, I should think.

Read More

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- EUR UAH PREDICTION

- Silver Rate Forecast

- Gold Rate Forecast

- DOT PREDICTION. DOT cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

- Core Scientific’s Merger Meltdown: A Gogolian Tale

2026-03-03 11:03