The markets, for the better part of seven years, have enjoyed a prosperity that borders on the artificial. The S&P 500 has delivered returns that, historically, are exceptional, almost suspiciously so. Such periods are rare; we have witnessed only a handful in the last century. The recent run, however, feels less like organic growth and more like a prolonged inflation of asset prices, a condition that cannot persist indefinitely.

The Dow Jones and the Nasdaq have, predictably, reached new heights. These numbers, though, are becoming detached from underlying economic reality. They are, in a sense, a measure of collective optimism, or perhaps, collective delusion. It is a dangerous game, this pursuit of ever-increasing valuations, and one that invites a reckoning.

There are, of course, headwinds. The market is, by any reasonable measure, expensive. The whispers of an artificial intelligence bubble grow louder. But these are, in the grand scheme of things, secondary concerns. The true challenge lies within the walls of the Federal Reserve.

Jerome Powell’s tenure concludes in May. His relationship with the previous administration was, shall we say, strained. It was evident that a change was inevitable. The nomination of Kevin Warsh, a former Governor, signals a departure from the prevailing orthodoxy. This is not merely a change in personnel; it is a potential shift in the very foundations of monetary policy.

Warsh, unlike his predecessor, views the central bank’s role with a degree of skepticism. He is, by inclination, a “hawk” – a term that, in the lexicon of finance, signifies a preference for restraint. He believes the Fed has overstepped its bounds, becoming an active participant in the markets rather than a neutral observer. This is a principled position, but one that is likely to provoke a considerable backlash.

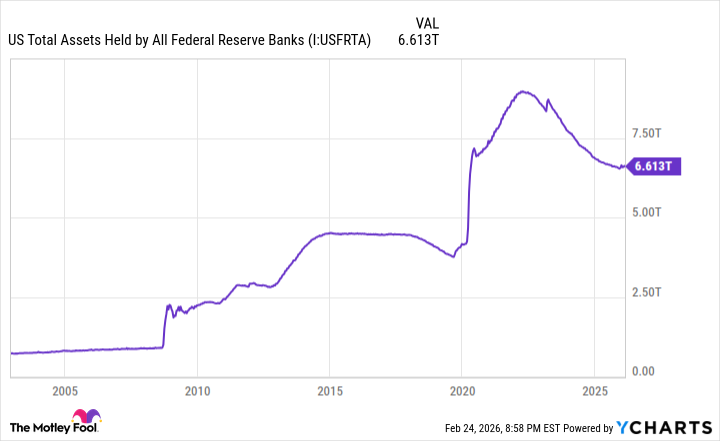

During the financial crisis, the Fed engaged in unprecedented interventions, purchasing trillions of dollars in Treasury bonds and mortgage-backed securities. This, Warsh argues, was a temporary measure that has become entrenched. He believes the Fed’s balance sheet must be significantly reduced. This, however, is not without risk. Reducing the money supply, even gradually, can lead to higher interest rates and a slowdown in economic growth. It is a delicate balancing act, and one that requires a degree of courage that is often lacking in those who hold positions of power.

The true challenge facing Warsh, however, is not merely technical. It is a crisis of credibility. The Federal Reserve, for decades, has been seen as a pillar of stability. But in recent months, cracks have begun to appear. Dissent within the Federal Open Market Committee (FOMC) is on the rise. Members are increasingly divided on the appropriate course of action. This is not a sign of healthy debate; it is a symptom of deeper malaise. A house divided cannot stand, and a central bank fractured by internal conflict is a dangerous thing indeed.

Powell, for much of his tenure, enjoyed a remarkable degree of consensus. Dissent was rare. But in the last few months, the tide has turned. Meetings that once produced unanimous decisions now yield multiple dissents, often in opposing directions. This is unprecedented. It suggests that the foundations of the Fed’s authority are crumbling.

Warsh’s task, should he be confirmed, will be to restore that authority. He must unify the FOMC and convince the markets that the Fed is once again a credible guardian of economic stability. This will not be easy. The markets are fickle and easily spooked. But if Warsh fails, the consequences could be severe. The continuation of the current bull market – a market that, by any rational measure, is overvalued – may depend on his success. The stakes, in other words, are exceedingly high.

Read More

- Top 15 Insanely Popular Android Games

- Gold Rate Forecast

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- EUR UAH PREDICTION

- Core Scientific’s Merger Meltdown: A Gogolian Tale

- Why Nio Stock Skyrocketed Today

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

- Silver Rate Forecast

2026-03-01 14:42