The market, dear friends, is a curious beast. It rewards momentum, naturally. But true momentum isn’t merely a rising share price; it’s a self-perpetuating engine, a flywheel if you will. A properly greased flywheel, mind you, not one rusted solid with optimistic accounting. We’ve been combing the exchanges, not for the obvious behemoths, but for companies with these subtle, spinning mechanisms. Companies that, shall we say, understand the art of turning a kopeck into a ruble… repeatedly.

Two such enterprises have caught our eye: MercadoLibre (MELI +1.01%) and Toast (TOST 1.51%). Both are currently trading at valuations that suggest either profound skepticism or, more likely, a temporary lapse in collective reason. A discerning investor, one who appreciates a well-constructed scheme, can capitalize on such moments.

MercadoLibre: The Latin American Emporium

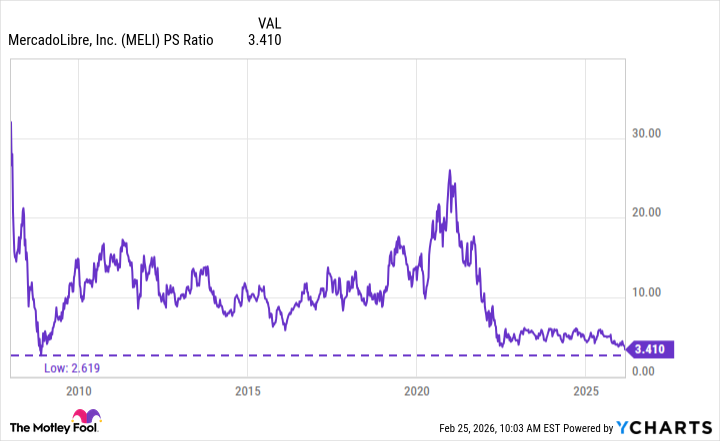

MercadoLibre, as of this writing, is experiencing a bout of market indigestion – a 34% dip from its peak. A temporary setback, we assure you. The flywheel, that ingenious device, continues to spin with admirable vigor. Twenty-eight consecutive quarters of over 30% revenue growth isn’t achieved through wishful thinking, but through a cleverly orchestrated ecosystem. They’ve built a digital bazaar, a financial network, and a logistics infrastructure, all feeding into each other. It’s a beautiful thing, really – a testament to the power of organized commerce.

Latin America, you see, is a continent ripe for disruption. And MercadoLibre, with its tentacles in e-commerce, fintech, credit, advertising, and logistics, is the octopus in question. The more they sell, the more they finance, the more they deliver, the more they… well, you get the picture. Their fintech arm, with a 27% monthly active user growth – a staggering 78 million users – is particularly intriguing. It’s not just about moving money; it’s about controlling the flow of capital, and that, my friends, is a position of considerable power. This, of course, fuels their gross merchandise volume, which enjoyed a robust 37% leap. A tidy sum, wouldn’t you agree?

Yet, the market remains unconvinced. The stock trades at a price-to-sales ratio not seen since the regrettable days of the Great Recession. A bargain, we say. A blatant oversight. The kind of opportunity that separates the astute investor from the mere speculator.

Toast: The Restaurant’s New Master

Now, some might object to MercadoLibre’s generosity with free shipping, citing a potential impact on profit margins. A valid concern, perhaps, for the faint of heart. But for those seeking a more… predictable margin profile, we present Toast. This company, specializing in technology for the restaurant industry, enjoys a delightful tailwind as it expands. They sell payment-processing hardware at a loss, a seemingly illogical practice. But it’s a calculated loss, a strategic investment in customer acquisition. A bit like offering a free glass of vodka to secure a long-term contract.

The real money, naturally, lies in the subscription software. A gross margin of 70% – a most agreeable figure – fuels the engine. In the fourth quarter of 2025, their annual recurring revenue hit $2 billion, growing 26% year over year. A substantial sum, wouldn’t you say? And, crucially, it’s a recurring sum. A predictable stream of revenue, like a well-maintained spring.

Toast’s strategy is elegantly simple. They gain traction in markets with high market share, leveraging brand recognition among restaurateurs. It’s a flywheel in action: acquiring new customers initially impacts profits, but retention unlocks the true potential of subscription services. A bit like planting a vineyard: initial investment, followed by years of fruitful harvests.

Management confidently predicts $10 billion in annual recurring revenue, which, at that scale, would generate substantial profits. With the stock down nearly 50% from its peak, trading at a mere 2.5 times sales, we believe Toast is a growth stock to acquire now. A perfectly reasonable price for a company with such promising prospects.

Growth, dear friends, is a most beneficial trait. MercadoLibre and Toast both possess the flywheels necessary to sustain that growth for the foreseeable future. And that, in our humble opinion, makes them both worthy investments. A bit of shrewd observation, a touch of calculated risk, and a healthy appreciation for the art of the deal – that’s all it takes. Remember, the market rewards those who understand the game. And we, my friends, are seasoned players.

Read More

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- EUR UAH PREDICTION

- Core Scientific’s Merger Meltdown: A Gogolian Tale

- Why Nio Stock Skyrocketed Today

- Gold Rate Forecast

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

- EUR TRY PREDICTION

- 4 Reasons to Buy Interactive Brokers Stock Like There’s No Tomorrow

2026-02-28 23:22