What people are watching on HBO and Max is always changing, and this week shows a wide range of popular choices. Viewers are tuning into everything from intense medical stories and funny takes on the news to fascinating true crime documentaries. Both established shows and brand new releases are attracting big audiences. Here’s a look at the top shows currently performing well on the platform, based on the latest viewership numbers. This list shows which programs are getting the most attention from viewers, combining scripted dramas and unscripted reality TV.

‘People Magazine Investigates’ (2016–)

As a true crime buff, I’ve been really hooked on ‘People Magazine Investigates.’ What sets this series apart is its deep dive into some of America’s most infamous and tragic cases. They don’t just rehash old news; they track down fresh interviews with the families affected, the officers who worked the cases, and the reporters who originally covered everything. Each episode feels like they’re genuinely trying to find new leads and, more importantly, bring some peace to the victims and their loved ones. The way they combine old news footage with insightful commentary makes it a must-watch for anyone who loves a good investigative series.

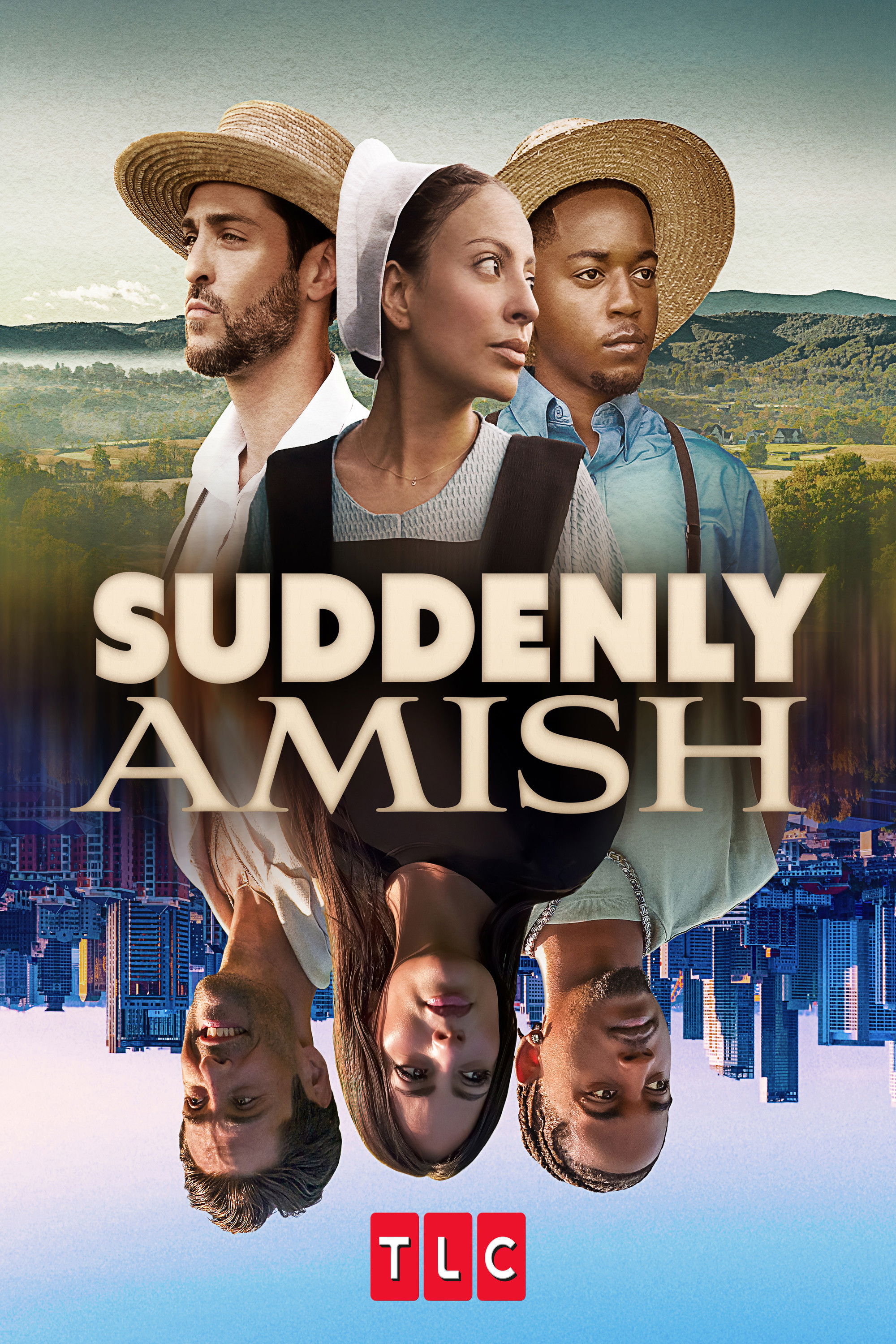

‘Suddenly Amish’ (2026)

‘Suddenly Amish’ documents the experiences of people who temporarily leave their modern lives to live as part of an Amish community. The show highlights the difficulties these individuals face as they adjust to the Amish way of life, which includes strict rules about technology, what they wear, and how they interact with others. Viewers see how challenging it is to live a life focused on hard work and religious beliefs. The series offers a fascinating comparison between modern society and traditional values.

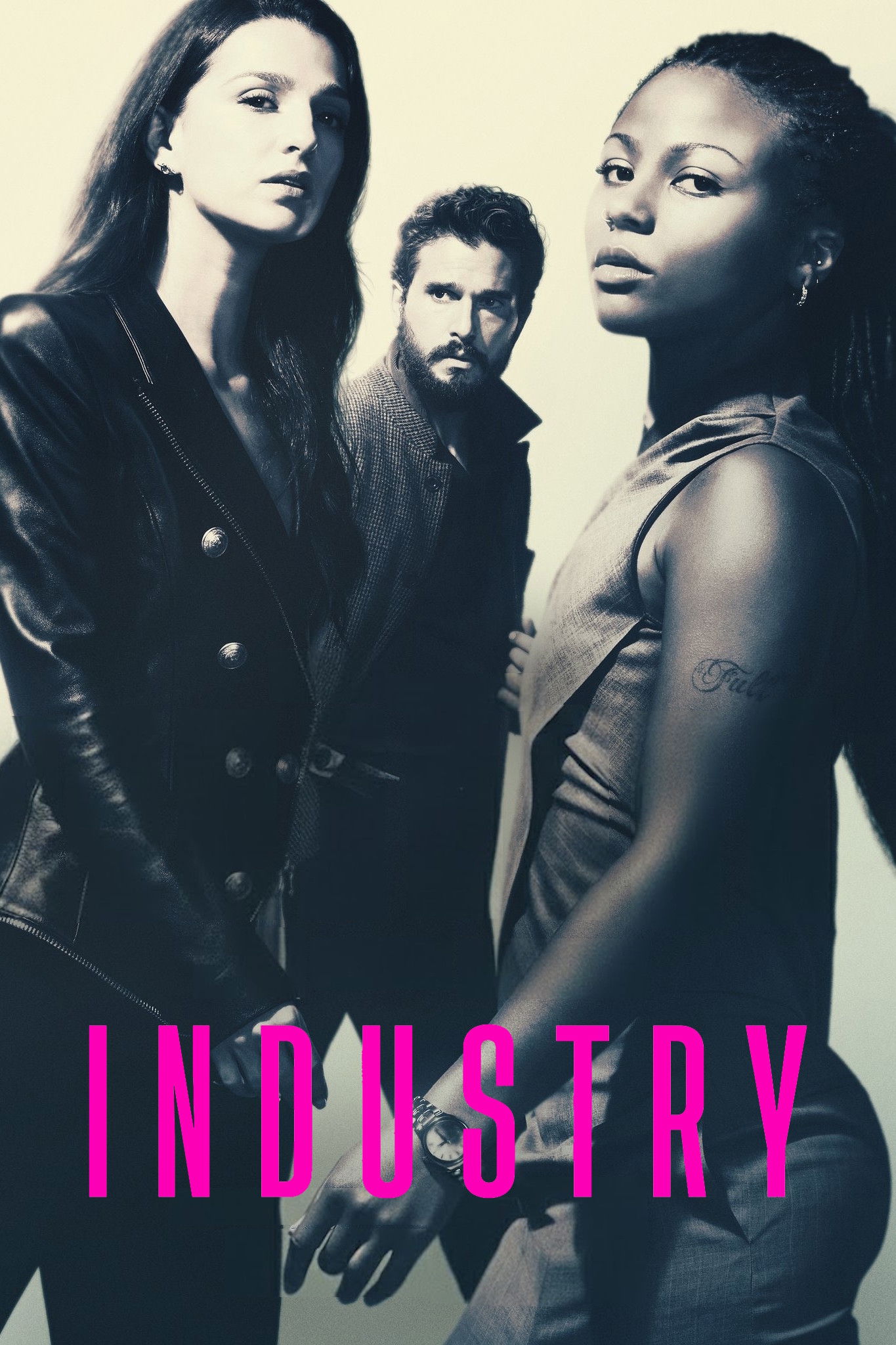

‘Industry’ (2020–)

Industry follows a group of recent graduates vying for full-time jobs at the high-powered investment bank, Pierpoint & Co, in London. The series dives into the competitive world of international finance, exploring themes of ambition, the pressures of work, and complicated relationships. As these young professionals navigate a demanding and ruthless corporate environment, they’re forced to confront how far they’ll go to achieve success. The show is known for its fast-paced action and realistic portrayal of the intense stress within the banking world.

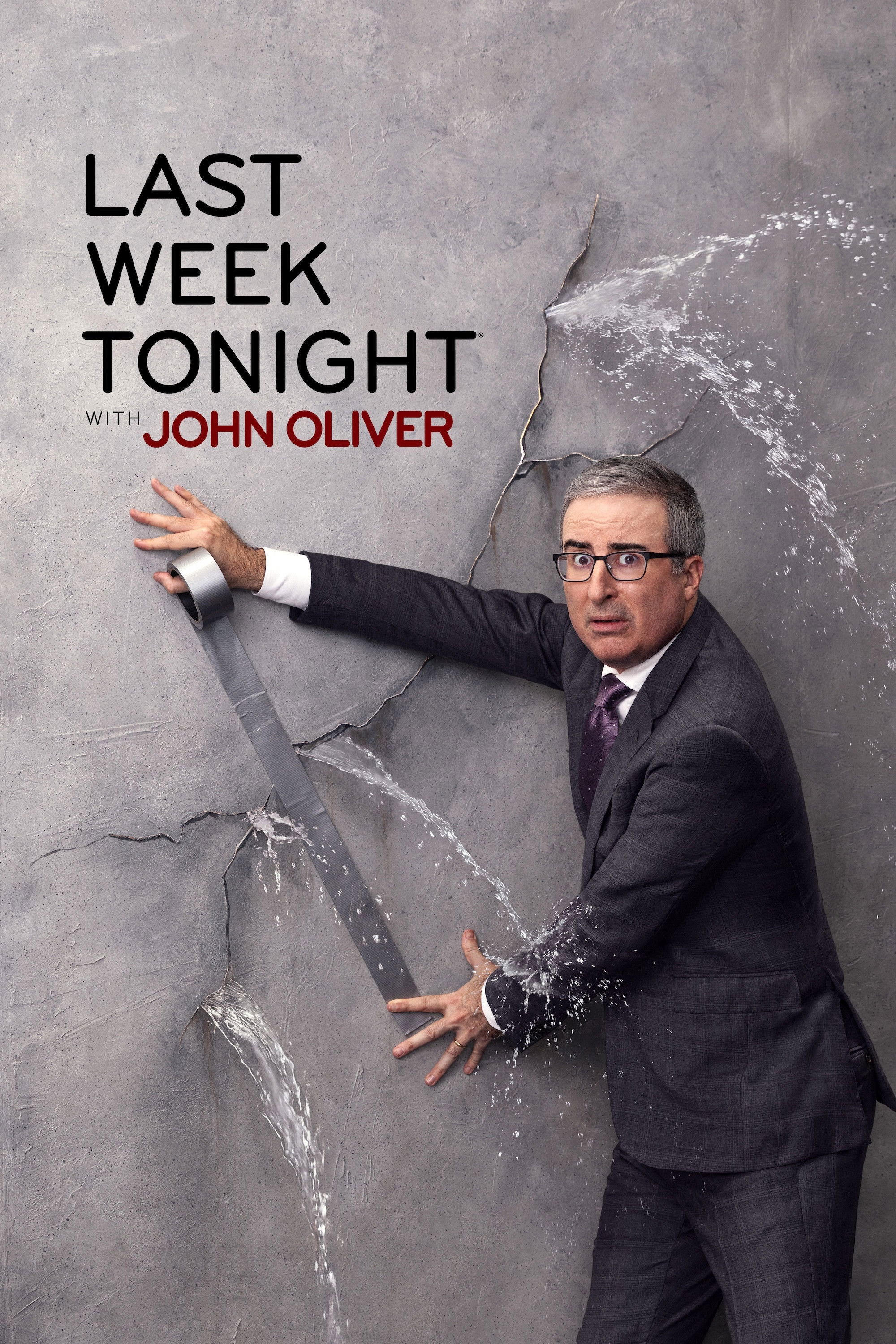

‘Last Week Tonight with John Oliver’ (2014–)

‘Last Week Tonight with John Oliver’ is a weekly talk show that uses satire to examine news, politics, and current events. Host John Oliver combines comedy with in-depth reporting to explain complicated topics, from powerful corporations to global issues. The show is famous for its detailed segments, which often spark public conversation and bring attention to important but often ignored problems. It’s one of the most award-winning talk shows on television, known for being both entertaining and informative.

‘1000-lb Sisters’ (2020–)

‘1000-lb Sisters’ follows Amy and Tammy Slaton as they try to lose weight and improve their health. The show details the challenges they face with their weight, including problems with movement and emotional struggles. Over the seasons, viewers see their efforts to get weight loss surgery and live healthier lives. It also emphasizes how important family support is, and how hard it can be to make big changes when everyone is watching.

‘Lost Women of Alaska’ (2026)

‘Lost Women of Alaska’ examines the mysterious disappearances and murders of women in the Alaskan wilderness. The series highlights the difficulties faced by law enforcement in this remote region, due to its challenging landscape and scattered communities. By revisiting old cases through interviews and updated forensic analysis, the show seeks to bring attention to these unsolved mysteries, honor the victims, and potentially provide answers for their families.

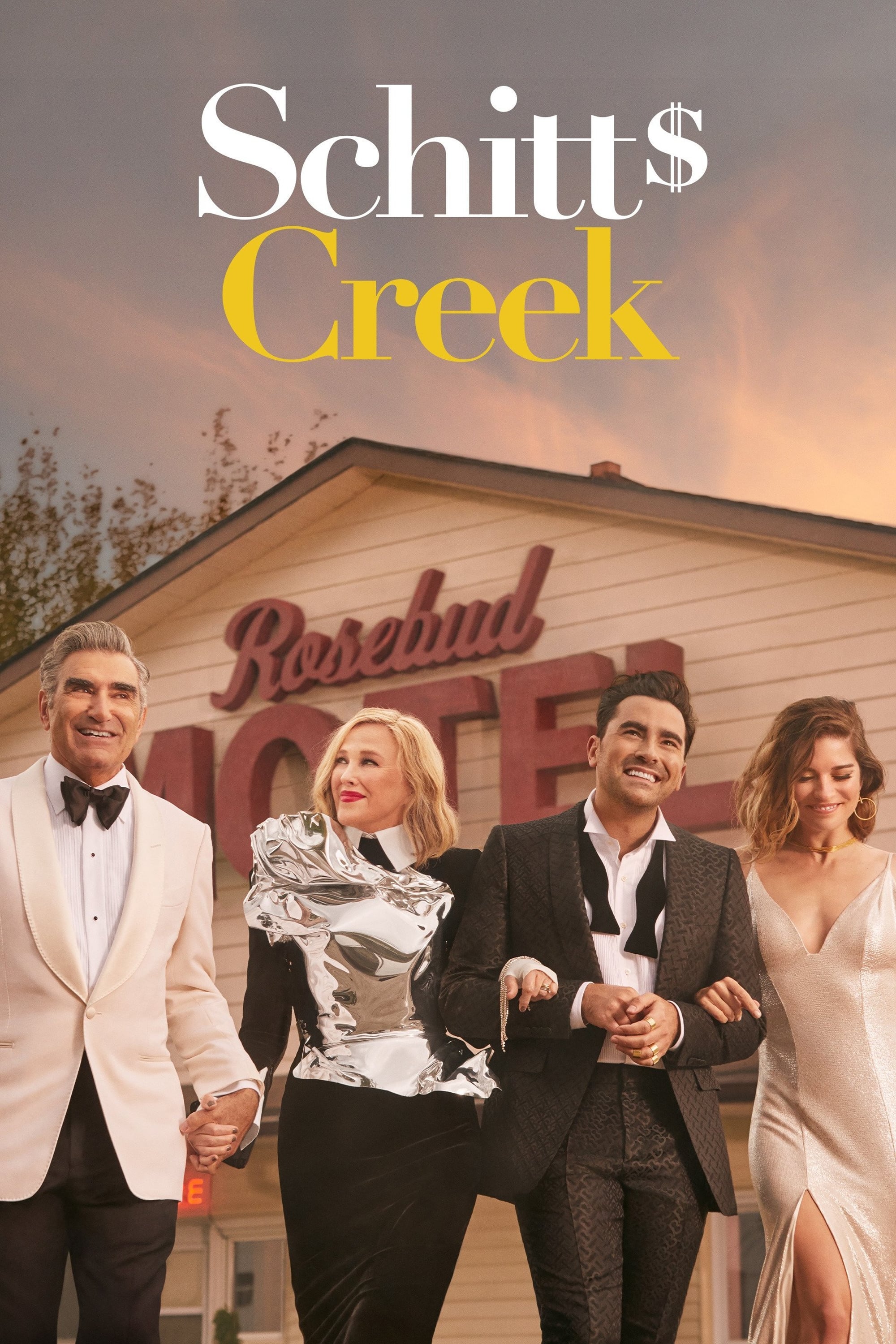

‘Schitt’s Creek’ (2015–2020)

‘Schitt’s Creek’ follows the Rose family, who suddenly find themselves broke after losing their vast fortune. They’re forced to move to a small, forgotten town they once purchased as a gag. The series shows how they adapt to a life without money, living in a simple motel and getting to know the town’s quirky residents. As they face challenges together, the family members form real bonds with the locals and with each other. The show became incredibly popular worldwide, earning praise and awards for its clever writing and well-developed characters.

‘Neighbors’ (2026)

‘Neighbors’ takes a look at the lives of people living in a picture-perfect suburban neighborhood where everyone seems to know each other’s business. But beneath the calm surface, the series reveals hidden tensions and secrets among the families. The show explores how easily small disagreements can grow into big problems when people live so close together. It’s a blend of drama and social observation, examining the challenges and difficult choices people face in their everyday lives.

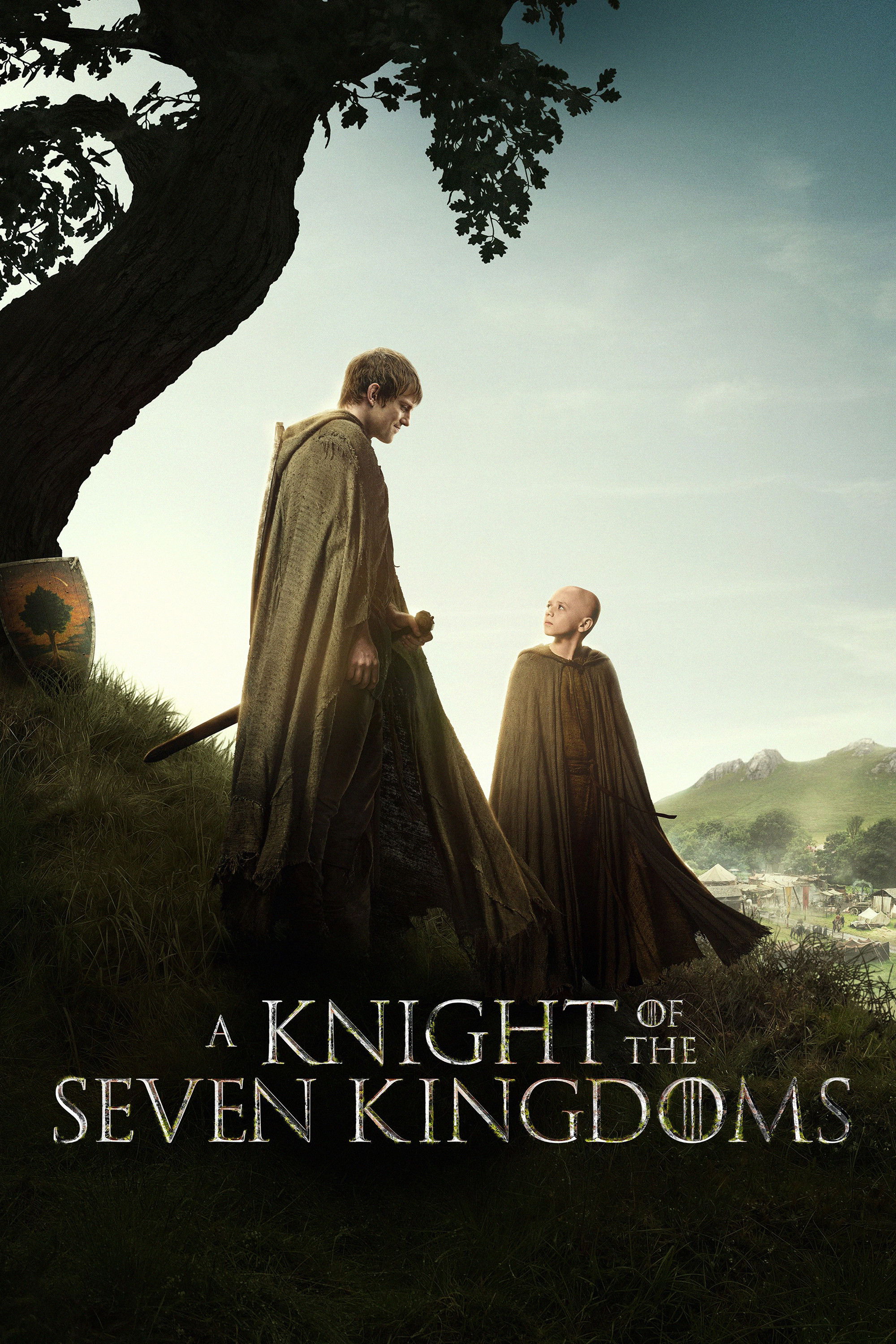

‘A Knight of the Seven Kingdoms’ (2026)

‘A Knight of the Seven Kingdoms’ is a prequel to ‘Game of Thrones’, meaning it takes place before the events of the original series. The show, inspired by writings from George R.R. Martin, centers on the story of Ser Duncan the Tall and his companion, Egg. Set about a hundred years earlier, it offers a look at Westeros during the time of the Targaryen family, with a focus on the characters and their personal stories within the larger history of the realm.

‘The Pitt’ (2025)

‘The Pitt’ is a medical drama set in a busy Pittsburgh hospital, realistically portraying the daily lives of doctors and nurses. The show explores the difficulties healthcare workers face with an overwhelmed system and challenging patients. Starring Noah Wyle, it’s a return to medical television for the actor, placing him in a high-stakes environment. The series offers a raw and honest look at the commitment and strength it takes to save lives in a major city hospital.

Please share your thoughts on these most-watched titles in the comments.

Read More

- Top 20 Dinosaur Movies, Ranked

- 20 Movies Where the Black Villain Was Secretly the Most Popular Character

- 25 “Woke” Films That Used Black Trauma to Humanize White Leads

- Silver Rate Forecast

- Spotting the Loops in Autonomous Systems

- Gold Rate Forecast

- Celebs Who Narrowly Escaped The 9/11 Attacks

- From Bids to Best Policies: Smarter Auto-Bidding with Generative AI

- 22 Films Where the White Protagonist Is Canonically the Sidekick to a Black Lead

- Can AI Lie with a Picture? Detecting Deception in Multimodal Models

2026-02-28 22:23