![]()

The market, that vast and often capricious entity, demands constant assessment. One observes the movements of capital, not as mere transactions, but as symptoms of a deeper malaise – a struggle for genuine value amidst the ephemeral illusions of progress. Mr. William Ackman, a practitioner of this demanding art, has recently adjusted his holdings, a course correction worthy of scrutiny. He has, with a measured hand, pruned from his portfolio a portion of his investment in Alphabet, while simultaneously augmenting positions in Amazon and Meta Platforms. This is not simply a trade, but a declaration – a judgment rendered upon the landscape of technological ambition.

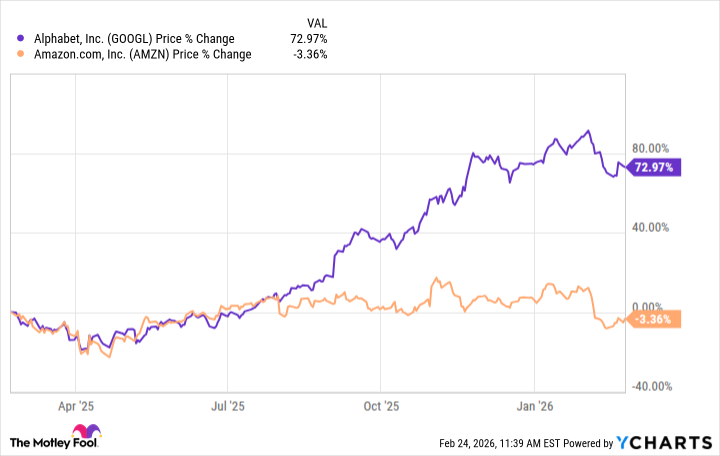

For some time, Mr. Ackman had allocated capital to Alphabet, a company once hailed as a harbinger of boundless innovation. The initial foray, acquiring shares of both Class A and Class C designations, represented a tentative acceptance of the prevailing narrative – that artificial intelligence would be the defining force of the coming decades. However, the act of reducing that position, by a substantial 86% for Class A shares and a more modest 2% for Class C, speaks volumes. It is the quiet withdrawal from a belief, a recognition that the promise of effortless returns, so readily advertised, rarely materializes without exacting a cost.

The Amazonian Consolidation

The redirection of capital toward Amazon is, at first glance, a continuation of the same thesis – a bet on the future of computation. Both Alphabet and Amazon, after all, are constructing vertically integrated ecosystems, each vying for dominance in the cloud infrastructure domain. Amazon Web Services, with its commanding 28% market share, holds a considerable advantage, while Alphabet’s Google Cloud trails in third place with 14%. This is not a contest of pure innovation, however, but a struggle for control – a consolidation of power over the very foundations of the digital realm.

The increasing reliance on proprietary silicon, mirroring the work undertaken by Broadcom for Alphabet, is a crucial detail. Amazon’s commitment to its Trainium and Inferentia chips is not simply a matter of cost reduction, but a deliberate attempt to break free from the dependence on Nvidia’s architectures. This is a strategic imperative, a recognition that true independence requires mastery of the underlying technology. It is a rejection of the notion that one can simply outsource innovation and expect to retain control.

Beyond the data centers and the cloud, the exploration of AI capabilities across consumer electronics, autonomous vehicles, robotics, and even quantum computing, is a testament to the boundless ambition of these corporations. But ambition, unchecked by prudence, is a dangerous force. The question is not merely what these companies can achieve, but at what cost to individual liberty and societal well-being.

The recent performance of Alphabet, with its considerable gains over the past year, likely influenced this reallocation. To realize profits after a period of appreciation is not inherently cynical, but a responsible course of action. Amazon, having experienced a more modest trajectory, presented a comparatively reasonable entry point. This is not market timing, precisely, but a pragmatic adjustment based on observable realities.

Meta: The Undervalued Contender

The addition of Meta Platforms to the portfolio, acquiring 2.7 million shares, is perhaps the most intriguing development. Meta, burdened by skepticism and haunted by the specter of its metaverse ambitions, has been largely dismissed by the prevailing narrative. Critics rightly point to the company’s reliance on advertising revenue and question the efficiency of its AI spending. Yet, beneath the surface, a different story is unfolding.

The Advantage+ product, operating at a reported $60 billion annual revenue run rate, is a significant achievement. This suite of tools, leveraging machine learning algorithms, is demonstrably improving the return on investment for Meta’s advertising customers. The potential for expanding Advantage+ across the company’s vast ecosystem – encompassing Facebook, Instagram, and WhatsApp, with over 3.6 billion daily active users – is considerable. This is not merely a technological advancement, but a consolidation of power over the attention economy.

The question remains: will Meta be able to leverage this advantage to command robust unit economics and drive higher engagement? The answer, as always, lies in the execution. But the potential is there, and it is being largely overlooked by a market fixated on short-term results.

A Measured Response to a Volatile Landscape

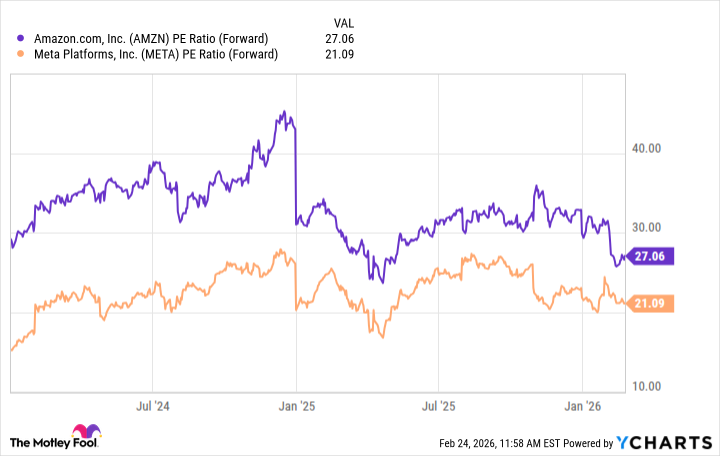

Both Amazon and Meta have experienced valuation corrections in recent months. Amazon’s announcement of materially higher capital expenditures in 2026 triggered a sell-off, while Meta remains in a “prove it to me” mode. This volatility, however, presents an opportunity for discerning investors. Both companies are now trading near their cheapest forward price-to-earnings ratios since the dawn of the AI revolution.

These dynamics suggest that the market is prioritizing near-term uncertainties over long-term potential. Institutional investors, like Mr. Ackman, appear to be taking a longer view, recognizing that both Amazon and Meta are well-positioned to benefit from the ongoing AI boom. To follow his lead, and acquire these holdings at a discounted price, may prove to be a prudent course of action for retail investors with a similar long-term horizon. It is not a guarantee of success, of course, but a reasoned response to a volatile landscape – a quiet assertion of faith in the enduring power of value amidst the relentless currents of change.

Read More

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- Why Nio Stock Skyrocketed Today

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- ETH PREDICTION. ETH cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- Superman Still Lost Money Theatrically Despite ‘Strong Performance’ in WB’s Q3 Earnings

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

2026-02-27 22:22