![]()

The semiconductor industry, you see, has been having a positively ripping good time of late. The PHLX Semiconductor Sector index, a rather dashing collection of enterprises, has surged a most agreeable 175% over the past three years. Quite a performance, what? And it leaves the S&P 500, which managed a respectable 70% jump, looking a bit like a slow-moving tortoise in comparison. One can’t help but feel a certain sympathy for the tortoise, naturally, but progress, as they say, is a relentless beast.

The reason for this exuberance, you see, is that semiconductors are rather like the oil of the modern age – essential building blocks for practically everything. From the motorcars we rattle about in, to the computing contraptions we tap away at, to those pocket telephones that seem to have glued themselves to everyone’s ear, and even the factories and data centers that keep the whole show running, almost everything relies on these little silicon chaps. Consequently, companies like Nvidia (NVDA 3.50%) and Taiwan Semiconductor Manufacturing (TSM 1.36%) have been making investors rather jolly indeed over the last three years. A most satisfactory state of affairs, wouldn’t you agree?

But if one were forced to choose between these two titans of the chip world for one’s portfolio, a tricky dilemma, what? Which one should a prudent investor favour? Let’s have a bit of a look-see, shall we?

Nvidia and TSMC Riding the AI Wave

Nvidia’s stock has positively rocketed, soaring over 700% in the last three years, while TSMC has also enjoyed a perfectly respectable climb of 311%. Nvidia’s exceptional performance is down to the phenomenal demand for its graphics processing units (GPUs), which are being snapped up by everyone from hyperscalers to governments, all eager to build and deploy AI infrastructure. A rather clever bit of engineering, those GPUs, what!

Meanwhile, TSMC, as the largest semiconductor foundry in the world, has been capitalizing on the general growth in chip demand. Companies like Nvidia, who design the chips but leave the actual manufacturing to foundries like TSMC, have inadvertently propelled the latter’s remarkable growth. A rather symbiotic relationship, wouldn’t you say?

Estimates suggest that TSMC is poised for a 34% increase in earnings in 2026, which is rather good, though not quite as spectacular as Nvidia’s anticipated 66% surge in fiscal 2027. Not surprising, really, considering Nvidia has cornered a massive 81% of the AI chip market. A rather dominant position, one might say.

Looking ahead, Nvidia is likely to continue its outstanding growth. The company anticipates investments in data centers to increase at a compound annual growth rate of 40% over the next five years. They believe annual data center capex could land between $3 trillion and $4 trillion by 2030. A rather substantial sum, wouldn’t you say? So, its dominant stature in AI chips is likely to pave the way for years of outstanding growth.

This lucrative data center opportunity also bodes well for TSMC. That’s because it manufactures chips not just for Nvidia, but also for other chip designers such as Qualcomm, Advanced Micro Devices, MediaTek, and a host of others. TSMC also makes chips that go into consumer devices such as personal computers, smartphones, and gaming consoles. A remarkably diversified operation, what!

All this indicates that TSMC is poised to benefit from more than just AI data center chips. But does this make it a better buy than Nvidia for the long run? A most pertinent question, indeed.

Which One Should Investors Be Buying?

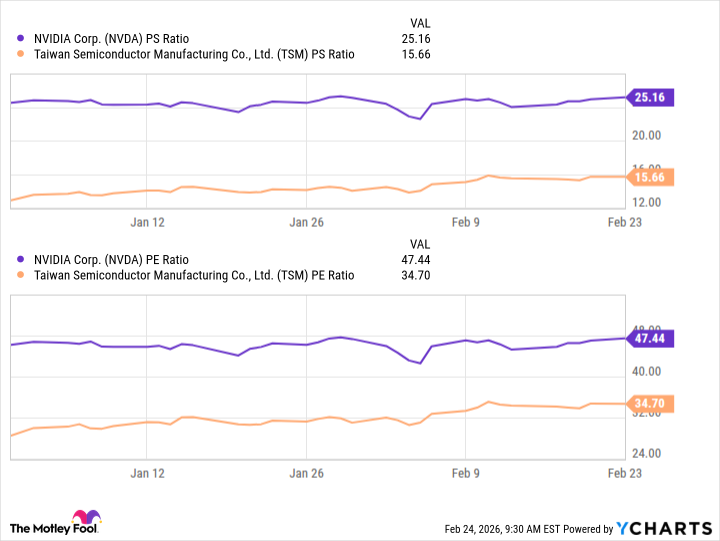

It can be said that AI has been the primary growth driver for both Nvidia and TSMC in recent years, and that catalyst is here to stay. Of course, TSMC’s 72% share of the global foundry market and its diversified customer base mean that it can benefit from AI adoption in multiple areas in the long run. And, importantly, TSMC is currently cheaper than Nvidia. A most agreeable circumstance for the value-conscious investor.

So, investors looking for a mix of value and growth can consider buying TSMC if they are looking to capitalize on the secular growth of the semiconductor market. A perfectly sensible course of action, wouldn’t you agree? It’s a bit like choosing between a rather dashing sports car and a reliable, well-appointed sedan – both will get you there, but one offers a bit more bang for your buck, and the other, a certain degree of dependability. A most satisfying investment, what!

Read More

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Top 15 Insanely Popular Android Games

- Did Alan Cumming Reveal Comic-Accurate Costume for AVENGERS: DOOMSDAY?

- Why Nio Stock Skyrocketed Today

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- ETH PREDICTION. ETH cryptocurrency

- ELESTRALS AWAKENED Blends Mythology and POKÉMON (Exclusive Look)

- Superman Still Lost Money Theatrically Despite ‘Strong Performance’ in WB’s Q3 Earnings

- New ‘Donkey Kong’ Movie Reportedly in the Works with Possible Release Date

2026-02-27 21:54