The current enthusiasm for all things Artificial Intelligence has, predictably, inflated a number of valuations. Ciena, a purveyor of optical networking components, has enjoyed a particularly buoyant twelve months, experiencing an increase of 176% in its share price. One is tempted to ask, not whether the company is thriving, but whether its investors are merely indulging in a particularly expensive game of make-believe.

The narrative, of course, is familiar. Massive investment in data centers, a veritable gold rush for those providing the infrastructure. From the silicon fabricators to the power suppliers, all are benefiting from the insatiable appetite for processing power. Ciena, it seems, is positioned to capture a portion of this largesse, providing the high-speed connections necessary to shuttle data across these digital landscapes. One might observe, however, that the history of technology is littered with companies that flourished on the back of a temporary trend, only to find themselves obsolete when the bubble burst.

The stock has, indeed, continued its ascent into 2026, currently boasting a 47% increase year-to-date. Gartner estimates a 32% jump in data center spending, reaching a sum that is, frankly, rather alarming. Ciena anticipates a revenue growth rate of 24%, a figure that, while respectable, hardly justifies the prevailing euphoria. The company speaks of a record backlog of $5 billion, a comforting statistic, though one wonders if this represents genuine demand or merely a pre-emptive stockpiling by clients anticipating further price increases.

Orders last year totaled $7.8 billion, exceeding revenue of $4.8 billion. A promising ratio, certainly, but one that invites scrutiny. The company’s management, with a characteristic lack of self-awareness, suggests that this demand will continue “into ’27 and beyond.” Such optimism is, one suspects, more about securing further investment than a realistic assessment of the market.

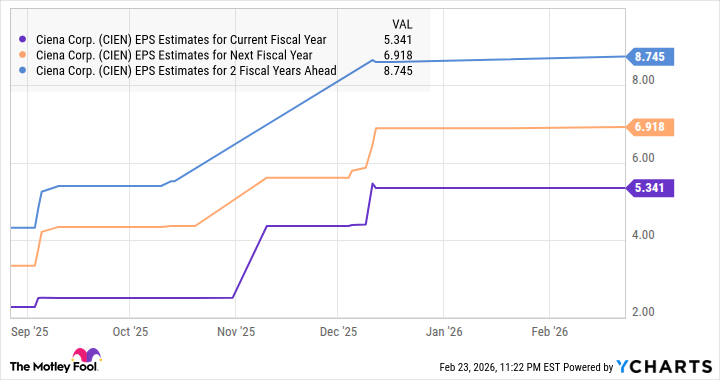

Earnings increased by 45% last year, reaching $2.64 per share. Analysts predict further gains. One is reminded of the old adage: the higher the monkey climbs, the more exposed his backside becomes. Ciena’s current valuation, at 40 times forward earnings, is, to put it mildly, ambitious. It dwarfs the forward earnings multiple of the Nasdaq-100, and significantly exceeds that of the S&P 500.

The company attempts to justify this premium by pointing to its potential for earnings growth. A doubling of earnings this year is predicted, well above the average for S&P 500 companies. One is tempted to ask: at what cost? And for how long? The current frenzy surrounding AI is, in many ways, reminiscent of the dot-com boom. Investors, eager to participate in the next big thing, are often willing to ignore fundamental principles of valuation.

For those seeking a growth stock to capitalize on the AI infrastructure spending, Ciena may indeed offer potential. However, investors should approach with caution. The company’s valuation is, to say the least, precarious. A more prudent course might be to observe from a safe distance, and wait for the inevitable correction. One should always remember that in the world of finance, the only constant is disappointment.

Read More

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- HSR 3.7 story ending explained: What happened to the Chrysos Heirs?

- ETH PREDICTION. ETH cryptocurrency

- Top 15 Insanely Popular Android Games

- Games That Faced Bans in Countries Over Political Themes

- Uncovering Hidden Groups: A New Approach to Social Network Analysis

- ‘Zootopia 2’ Wins Over Critics with Strong Reviews and High Rotten Tomatoes Score

- Best Ways to Farm Prestige in Kingdom Come: Deliverance 2

2026-02-27 17:02