![]()

Now, one observes a rather spiffing development in the world of artificial intelligence, don’t you know. It appears that the chaps building these digital brains are preparing to spend a positively colossal sum on the necessary infrastructure. Futurum, a firm that keeps a shrewd eye on these things, predicts that the five leading cloud providers will be parting with somewhere between $660 and $690 billion this year. A truly staggering amount, what! Considerably more than the $380 billion they splashed out last year. And that’s before one even considers the ambitious projects and the new players, like OpenAI and their ilk, adding to the tally. A most agreeable situation for those of us with a nose for a promising investment, wouldn’t you say?

It strikes me as perfectly clear that we’re on the cusp of another boom, and it’s those providing the foundational hardware who stand to benefit most handsomely. Two firms, in particular, have caught my discerning eye: Micron Technology (MU 3.20%) and Jabil (JBL 1.73%). Rather like a resourceful valet anticipating his master’s every need, these companies are poised to profit from the surging demand. Let’s have a closer look, shall we?

Micron Technology: Solving a Rather Tricky Problem

You see, these modern contraptions – these AI data centers – require a prodigious amount of memory. Micron’s dynamic random-access memory, or DRAM as the chaps in the know call it, plays a rather crucial role. Specifically, a high-bandwidth variety known as HBM. It allows these AI accelerators to quickly access the mountains of data they require. Without it, the whole shebang slows to a distinctly uninspiring crawl. It’s a bit like trying to run a marathon in lead boots, you see.

Micron, with a touch of foresight back in 2019, predicted that AI servers would need six times the DRAM of standard servers. A rather bold claim, one might think, but it appears to be spot on. Companies like Nvidia, those ingenious chaps, are cramming more and more memory into their AI chips, and Micron is there to supply it. Their new Vera Rubin processors, due to launch this year, will pack close to 300 gigabytes of HBM. Up from 200 gigabytes in the previous model. A most impressive feat of engineering, wouldn’t you agree?

This surge in demand has, naturally, led to a rather acute shortage of memory chips, allowing manufacturers to, shall we say, adjust their pricing. Bloomberg reported a 75% jump in the price of one variety of DRAM from December to January. A most agreeable turn of events for Micron, one imagines. And with the continued investment in AI infrastructure and the inherent difficulty in building new chip production capacity, this trend seems set to continue. Analysts, those shrewd observers, are becoming increasingly bullish about Micron’s earnings prospects, and one can hardly blame them.

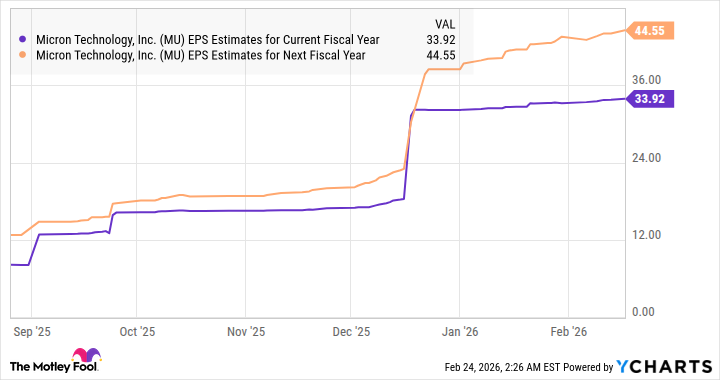

As the chart rather neatly illustrates, analysts are predicting a substantial increase in Micron’s bottom line. From $8.29 per share to, well, a figure that rather takes one’s breath away. A five-fold jump in just two fiscal years! A most tempting prospect for any investor with a modicum of sense. And the valuation? A mere 24 times trailing earnings and 12 times forward earnings. A positively bargainous price, wouldn’t you say? The Nasdaq-100, by comparison, trades at a considerably higher multiple. One might suggest grabbing a few shares before the price takes flight.

Jabil: A Hidden Gem, What!

Now, Jabil may not be a household name in the AI infrastructure game, but the company is quietly making a rather significant impact. They provide manufacturing, engineering, and supply chain services to a variety of industries, including automotive, healthcare, and, crucially, data centers. A most versatile firm, wouldn’t you say?

Management has noted that AI is now their primary growth driver. They engineer and build AI server racks, liquid-cooled servers, and power management solutions for AI data centers. A rather clever niche, wouldn’t you agree? They’ve launched new server products to capture the burgeoning demand, and they’re investing a substantial $500 million to expand their AI data center infrastructure manufacturing capacity. A most ambitious undertaking, what!

And it’s paying off handsomely. They’re now guiding for a 35% increase in AI revenue in fiscal 2026, reaching $12.1 billion. An improvement on their previous forecast of 25%. The stronger contribution from AI has also encouraged them to raise their operating margin guidance. A most agreeable development, wouldn’t you say?

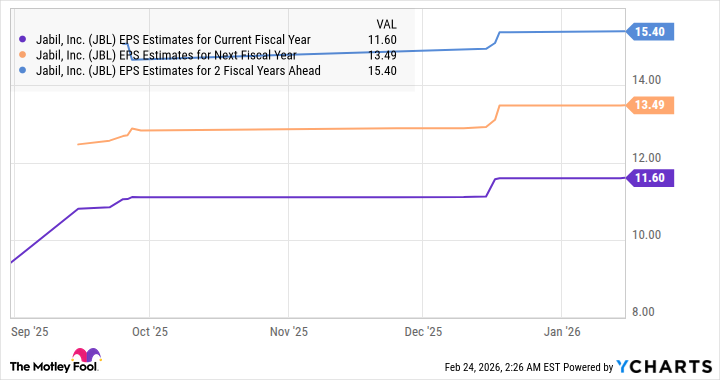

Analysts are forecasting robust double-digit percentage earnings growth, as the chart illustrates. The AI server market is expected to grow at an annualized rate of 34% through 2030. A most promising outlook, wouldn’t you agree? And the valuation? A mere 19 times forward earnings. A discount to the Nasdaq-100’s multiple. One might suggest that investors can acquire Jabil stock at an attractive price. The stock has jumped 33% over the past three months, but the points above suggest that there is still room for further upside. A most agreeable prospect, wouldn’t you say?

Read More

- Gold Rate Forecast

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- HSR 3.7 story ending explained: What happened to the Chrysos Heirs?

- ETH PREDICTION. ETH cryptocurrency

- ‘Zootopia+’ Tops Disney+’s Top 10 Most-Watched Shows List of the Week

- Here Are All the Movies & TV Shows Coming to Paramount+ and Apple TV+ This Week, Including ‘The Family Plan 2’

- Top 15 Insanely Popular Android Games

- The Labyrinth of Leveraged ETFs: A Direxion Dilemma

- Uncovering Hidden Groups: A New Approach to Social Network Analysis

2026-02-27 13:32