Oracle. The name itself sounds like a prophecy, doesn’t it? Or maybe that’s just the three cups of lukewarm coffee talking. I’ve been watching this stock for a while now, and it’s less a company and more a particularly elaborate Rube Goldberg machine. A beautiful, terrifying Rube Goldberg machine built on debt and the promise of…well, everything. My accountant, a man who usually reserves emotion for tax audits, actually raised an eyebrow when I mentioned it. That’s saying something.

It’s gone from being the dependable, slightly dusty software provider your dad’s office used, to the darling of Wall Street, and then, in what felt like a particularly swift plummet, to the poster child for high-risk AI spending. Honestly, it’s exhausting just keeping up with the narrative. It’s currently down 54.9% from its peak last September. Which, if you’re a glass-half-empty type – and let’s be honest, after a few years in this business, you tend to be – feels less like a buying opportunity and more like a warning.

The pitch, of course, is irresistible. Oracle wants to be the fourth major cloud player, joining Amazon, Microsoft, and Alphabet. They’re aiming for $144 billion in cloud revenue by 2030, up from $18 billion. That’s…ambitious. It’s the kind of ambition that keeps me awake at night, not because I’m excited, but because I’m calculating the potential for catastrophic failure. Amazon Web Services, the current leader, did $128.7 billion last year. So, Oracle is predicting they’ll surpass AWS in less than five years. It’s a lovely thought, really. Like believing you can win the lottery while simultaneously being audited by the IRS.

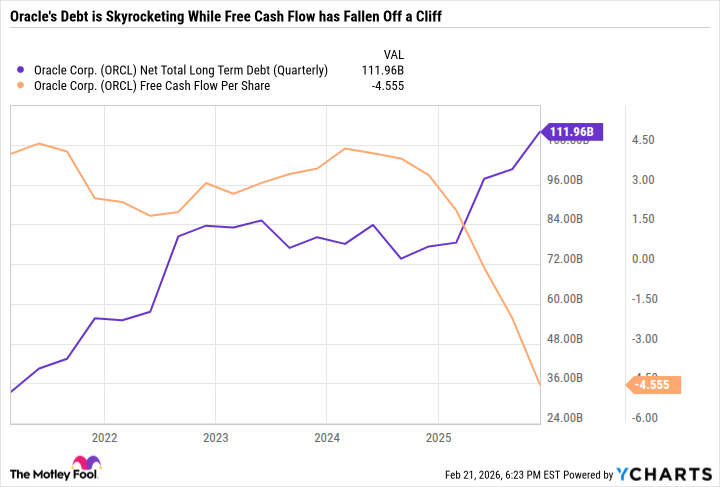

The thing is, Oracle’s database and data management software does generate a lot of free cash flow. It’s just…not enough to fund this cloud infrastructure binge. They’re spending money as if there’s no tomorrow, which, if this whole thing goes south, there might not be. At least, not for my portfolio. My sister-in-law, who thinks she’s a stock whisperer because she once correctly predicted the price of avocados, keeps telling me it’s a sure thing. I’m starting to suspect she’s deliberately trying to ruin me.

Their projections are heavily reliant on something called Remaining Performance Obligations, or RPO. Basically, it’s a backlog of orders. A very large backlog. But a significant chunk of that – around $300 billion – is tied to OpenAI. OpenAI! It’s like building a house on a foundation of hype and hoping the tide doesn’t come in. They’re also raising money through debt and equity, which, while not inherently bad, feels a little like applying a bandage to a severed artery.

Look, I’m not saying Oracle is doomed. I’m just saying it’s a gamble. A big, expensive, potentially catastrophic gamble. If you’re a risk-averse investor – the type who prefers a comfortable dividend yield to the thrill of potentially doubling your money – stick with Microsoft or Amazon. They’re not as exciting, perhaps, but they’re also less likely to give you a heart attack.

Oracle will report earnings soon. I won’t be looking for a bigger RPO number. I’ll be watching their spending, their cash burn, and their plan to get their balance sheet back in order. I’ll also be bracing myself. Because, honestly, watching this stock is starting to feel less like investing and more like a particularly stressful form of performance art. And my accountant? He’s already started looking at offshore accounts. Just in case.

Read More

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- Brown Dust 2 Mirror Wars (PvP) Tier List – July 2025

- Banks & Shadows: A 2026 Outlook

- HSR 3.7 story ending explained: What happened to the Chrysos Heirs?

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- ETH PREDICTION. ETH cryptocurrency

- The Best Actors Who Have Played Hamlet, Ranked

- Gay Actors Who Are Notoriously Private About Their Lives

- 9 Video Games That Reshaped Our Moral Lens

2026-02-25 15:12