It is, of course, a vulgar notion to believe that progress is measured solely in kilowatt-hours. Yet, even the most ardent aesthete cannot deny the growing thirst of our modern world. The latest reports suggest that data centers, those temples of digital vanity, already consume a rather alarming 4.4% of all electricity generated in the United States. And artificial intelligence, that most ambitious of human follies, threatens to demand enough power to illuminate 22% of American households by 2028. A truly dazzling prospect, if one ignores the inevitable bills.

The United States, in a moment of practical, if uninspired, foresight, has turned its gaze towards nuclear power. A commendable ambition, though one must wonder if it is driven by genuine concern for the future, or merely a desire to avoid the inconvenience of darkness. The Department of Energy, with the audacity of a benevolent despot, has decreed a tripling of American nuclear energy production by mid-century. A grand gesture, certainly, though one hopes it doesn’t involve too much drab concrete.

And what, pray tell, fuels these atomic ambitions? Uranium, naturally. Unlike so many fleeting trends, uranium possesses a certain enduring quality. While other energy resources have succumbed to the whims of the market, uranium’s spot price has, with admirable defiance, climbed 38% in the past year. A quiet triumph, if ever there was one.

However, unlike coal, which arrives in a conveniently combustible state, uranium requires a touch of refinement. It is here that Centrus Energy, a name that lacks a certain poetic flair, enters the stage. They don’t simply extract uranium; they enrich it, a process that sounds suspiciously like improving one’s social circle.

Enriching Uranium, Enriching Investors

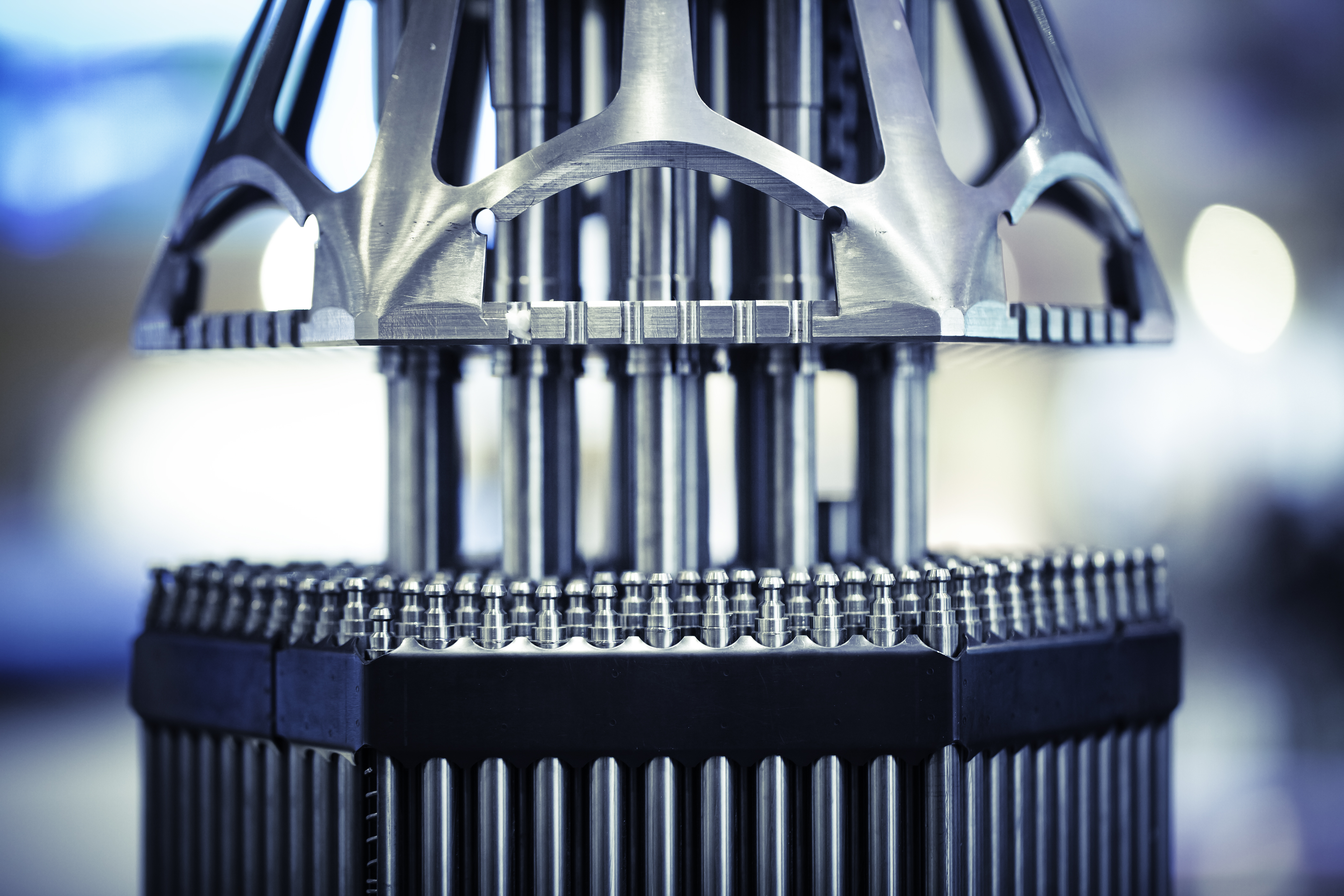

Centrus, denoted by the rather uninspired ticker symbol LEU, deals in the subtle art of uranium enrichment. They take ‘yellow cake’ – a name that suggests a particularly unfortunate dessert – convert it into UF6 gas, and then, with a precision that would delight a Swiss watchmaker, increase the concentration of U-235. This, for the uninitiated, is the isotope that makes nuclear fuel…functional. It is the very essence of power, distilled into a gaseous form. The result is light enriched uranium (LEU), the humble foundation of all those glowing reactors.

They are, remarkably, the only Nuclear Regulatory Commission-licensed producer of high-assay low-enriched uranium (HALEU). A rather cumbersome title, but one that suggests a certain degree of exclusivity. HALEU, it seems, allows for smaller reactors, which is all very well, though one hopes they don’t sacrifice grandeur for efficiency.

Centrus operates two plants, supplemented by a corporate headquarters in Bethesda, Maryland. The Oak Ridge facility, a rather utilitarian name, manufactures AC100M centrifuge machines – the very engines of enrichment. These machines, in turn, are deployed at the Piketon, Ohio plant, where the magic of LEU and HALEU truly happens.

And, naturally, they are investing heavily in both facilities. A $560 million investment in Oak Ridge, followed by a multibillion-dollar expansion of the Ohio plant, in partnership with Fluor. One might say they are doubling down on the future, though one suspects it is also a rather profitable endeavor.

Through its LEU business segment, Centrus provides the essential enrichment element for commercial nuclear reactors. They have a long-standing agreement with France’s Orano, and a contract with Russia’s TENEX, which, alas, expires next year. One wonders if geopolitical considerations will complicate matters. It always does, doesn’t it?

The Department of Energy, in a moment of decisive action, selected Centrus for a $900 million HALEU order. And they have agreements with ICHNP, Oklo, TerraPower, and X-energy. A veritable constellation of nuclear ambition.

The result, predictably, has been solid, steady growth. Annual net income grew by 5.6% in the past year, and revenue has enjoyed a 13% compound annual growth rate from 2020 to 2025. Their backlog of LEU sales agreements now stands at a rather impressive $2.3 billion.

Their cash reserves have nearly tripled, from $671.4 million to $1.95 billion. Total debt stands at $1.17 billion, leaving them with a healthy balance sheet and an eagerness to invest in their manufacturing capabilities. A commendable display of financial prudence, though one suspects it is also a rather astute business strategy.

There was, of course, considerable demand for Centrus’ LEU even before the current frenzy surrounding data centers. But they are taking all the right steps to emerge as America’s premier uranium enricher over the next few years. And that, my dear readers, makes it worth a look. The company’s strong bottom line has me thinking it’s not just hype, even after the company’s 83% surge over the past 12 months. A truly dazzling performance, though one hopes it doesn’t lead to an inflated sense of self-importance.

Read More

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- Brown Dust 2 Mirror Wars (PvP) Tier List – July 2025

- Banks & Shadows: A 2026 Outlook

- Gemini’s Execs Vanish Like Ghosts-Crypto’s Latest Drama!

- ETH PREDICTION. ETH cryptocurrency

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- HSR 3.7 story ending explained: What happened to the Chrysos Heirs?

- Top gainers and losers

- HSR Fate/stay night — best team comps and bond synergies

2026-02-24 16:12