what forces will ultimately determine the trajectory of this peculiar enterprise?

The Expenditure of Kingdoms

As of the year 2026, the pursuit of artificial intelligence resembles nothing so much as a frantic race towards an unknowable horizon. The great tech principalities – Amazon, Alphabet, and others – are expending fortunes, sums that would once have financed entire kingdoms, on ‘data centers’ – vast repositories of calculation. Amazon, for example, has declared its intention to increase its capital expenditures by a staggering 50%, reaching a total of 200 billion units of currency. Alphabet’s ambitions are comparable, earmarking between 175 and 185 billion. The estimates suggest that the total expenditure on artificial intelligence this year alone could exceed 700 billion. A prodigious sum, indeed.

These entities possess the means to sustain such spending, drawing upon diversified and profitable ventures. However, the wisdom of such an investment remains… debatable. Every expenditure represents an opportunity foregone, a path not taken. The value of this investment, furthermore, is shrouded in uncertainty. While the technology of artificial intelligence advances at an impressive rate, it consistently falls short of human performance in even the most basic of tasks. The companies that rent computing power from Nvidia’s clients – OpenAI and Anthropic, among others – are, by all accounts, operating at a substantial loss.

The market, that fickle deity, has begun to express its displeasure. Following Amazon’s announcement, its share price experienced a precipitous decline of nearly 20%. This suggests that investors are growing wary of the seemingly endless cycle of expenditure. Should this trend continue, it could compel these entities to curtail their spending or seek alternative solutions – perhaps the development of proprietary chips, designed to bypass the need for Nvidia’s hardware altogether.

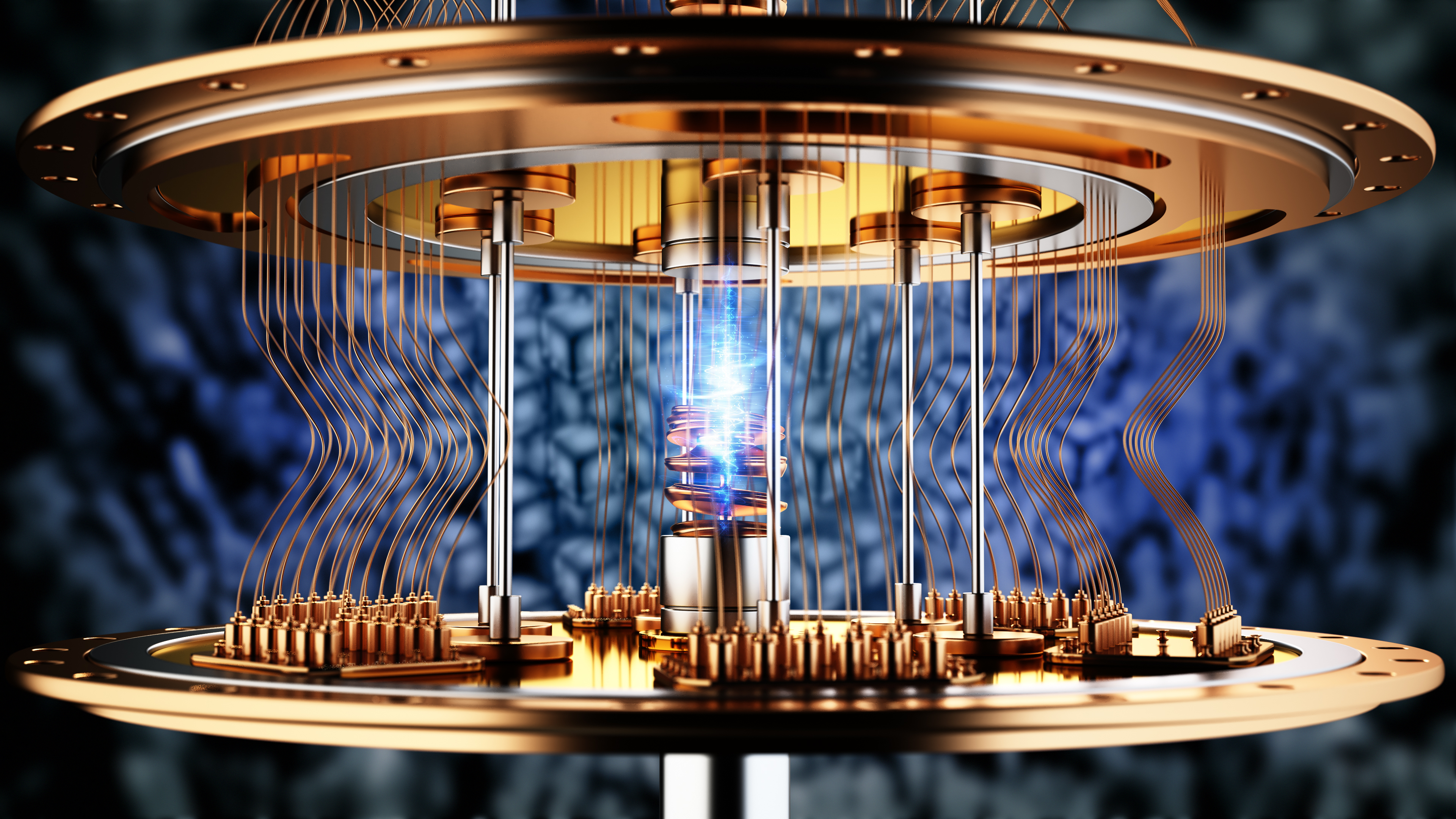

The Promise of New Labyrinths

Currently, approximately 90% of Nvidia’s revenue is derived from its ‘data center’ segment. This concentration of risk is… concerning. The company is, in effect, placing all its faith in a single, volatile market. However, management is actively seeking to diversify its revenue streams, exploring new frontiers of computation.

Nvidia has begun to invest heavily in ‘quantum computing,’ a field that promises to unlock computational possibilities previously confined to the realm of speculation. In October, the company announced ‘NVQlink,’ an architecture designed to couple its GPUs with quantum computers. It is, of course, too early to predict the outcome of this endeavor. However, analysts anticipate that quantum computing will become commercially viable by the end of the decade. Nvidia, with its expertise in chip design and its partnerships with manufacturers like Taiwan Semiconductor Manufacturing, appears well-positioned to capitalize on this opportunity.

The company also sees potential in ‘automotive hardware’ and ‘robotics,’ providing chips to assist with self-driving vehicles. This segment, while currently modest, generated $592 million in revenue in the third quarter, representing a growth of 32% year-over-year. As self-driving technology becomes more widespread, this segment could experience further acceleration.

The Speculation Continues

Over the next decade, new opportunities like quantum computing and automotive hardware could potentially offset a slowdown in demand for AI data center solutions. However, given that approximately 90% of Nvidia’s sales currently originate from its data center segment, it is questionable whether these new revenue streams will be sufficient to significantly alter the company’s trajectory.

That said, the company’s current valuation appears to account for these long-term challenges. With a forward price-to-earnings (P/E) multiple of just 24, the stock appears relatively inexpensive for a company that has experienced such rapid earnings growth – 67% year-over-year, reaching $1.30 per share in its most recent quarter. This low valuation provides a degree of safety as the company navigates these uncertain times. At present, a ‘hold’ rating appears to be the most prudent course of action, pending further clarification of the company’s prospects.

Read More

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- Brown Dust 2 Mirror Wars (PvP) Tier List – July 2025

- Banks & Shadows: A 2026 Outlook

- Gemini’s Execs Vanish Like Ghosts-Crypto’s Latest Drama!

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- HSR 3.7 story ending explained: What happened to the Chrysos Heirs?

- ETH PREDICTION. ETH cryptocurrency

- The Weight of Choice: Chipotle and Dutch Bros

- Top gainers and losers

2026-02-24 10:22