Well, I say, old bean, it appears that Bitcoin has found itself in a bit of a pickle, perched precariously at what one might call a “critical point.” The chaps in the trading trenches are divided, you see, between two rather familiar scripts: a full-on capitulation, the sort that leaves one feeling rather like a deflated whoopee cushion, or the early innings of a bottoming process as durable as a Jeeves-approved valet service. In a video explainer on Feb. 15, CryptoQuant’s Maartunn-a fellow who seems to know his onions-argued that the data is starting to align with the latter, though he’s quick to add that any bottom is more likely to be a grind than a snapback. Rather like trying to extricate oneself from a particularly sticky social engagement, what?

Is Bitcoin’s Bottom In, or Are We Still in the Soup?

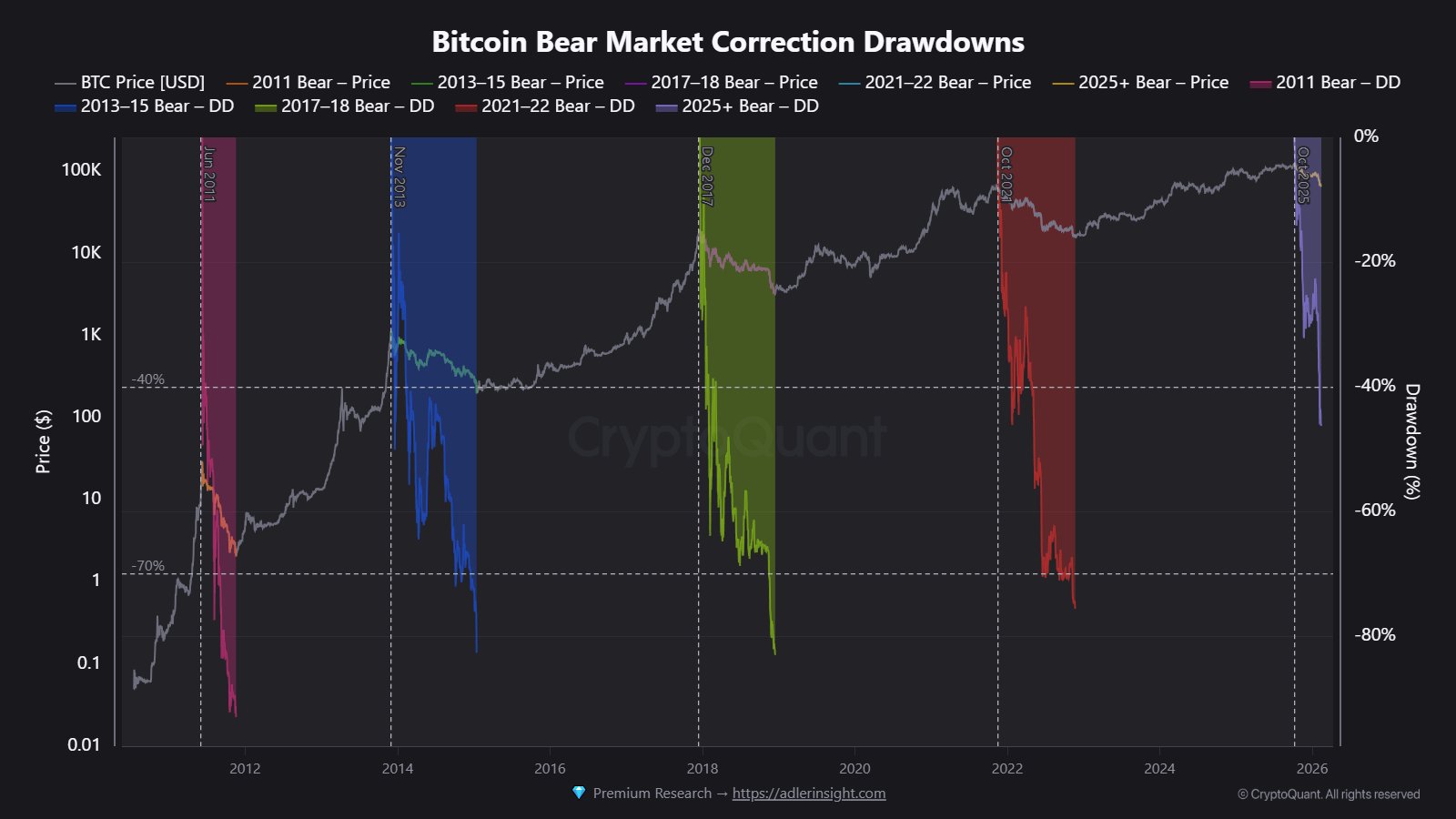

At present, Bitcoin is trading roughly 50% below its all-time high, a drawdown that looks rather severe when taken in isolation, but still a far cry from the 70%+ declines seen in previous bear markets, according to Maartunn. The more pressing question, he posits, is not whether the market can sink lower-though it very well might-but whether the ingredients for a turn are beginning to simmer. Rather like checking if the cook has remembered the key ingredients for a decent curry, eh?

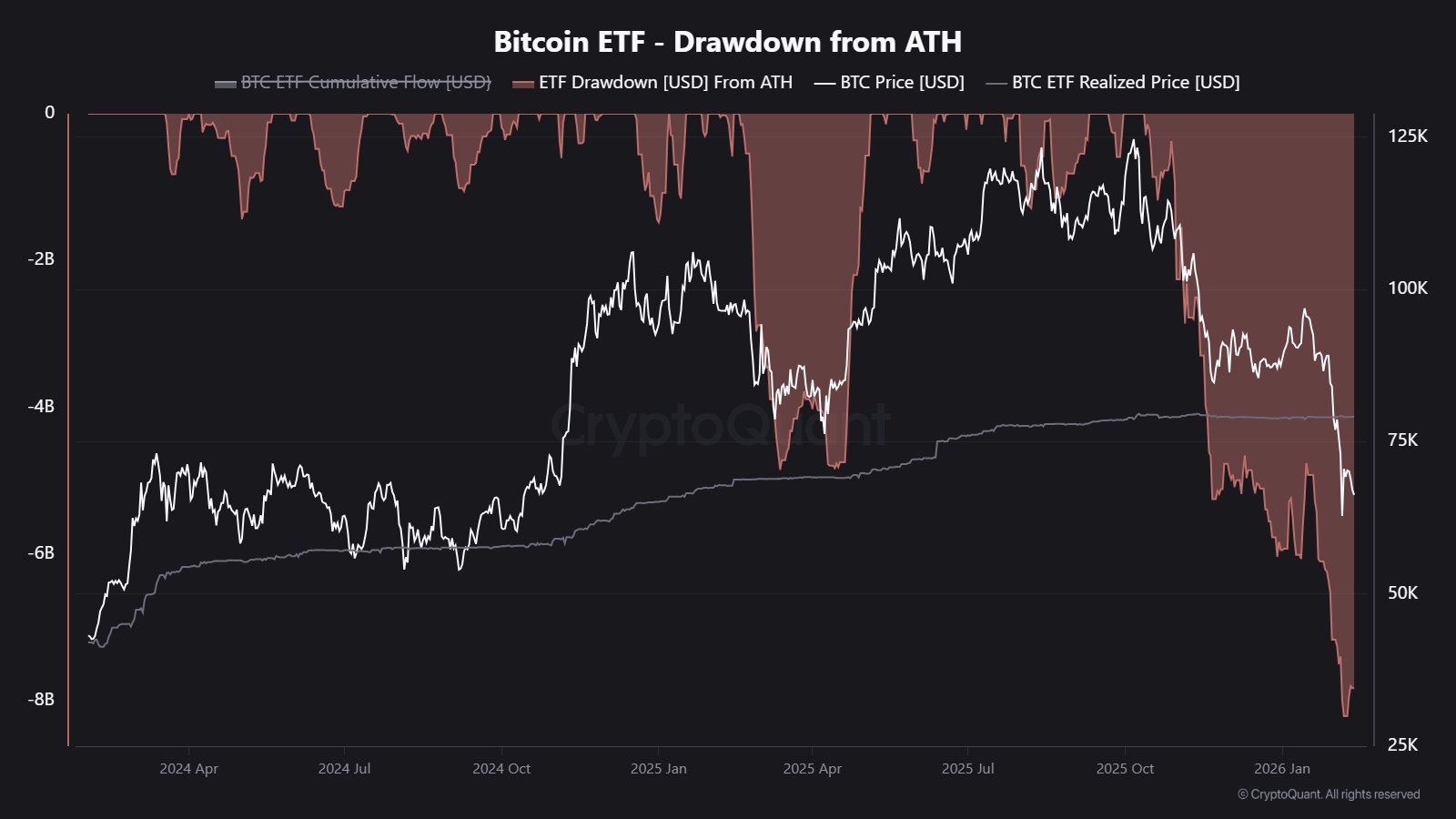

Maartunn points to what he calls “structural selling pressure” tied to spot ETFs. Apparently, these new spot ETFs have posted an $8.2 billion drawdown from peak holdings, “the largest on record,” creating a persistent sell pressure. It’s rather like having a house guest who keeps raiding the larder, leaving one’s supplies rather depleted. He adds that the current price is around 17% below the average buying price for ETF holders, putting a meaningful slice of that cohort underwater and potentially incentivized to cut their losses. Not exactly the sort of thing one wants to hear at the club, what?

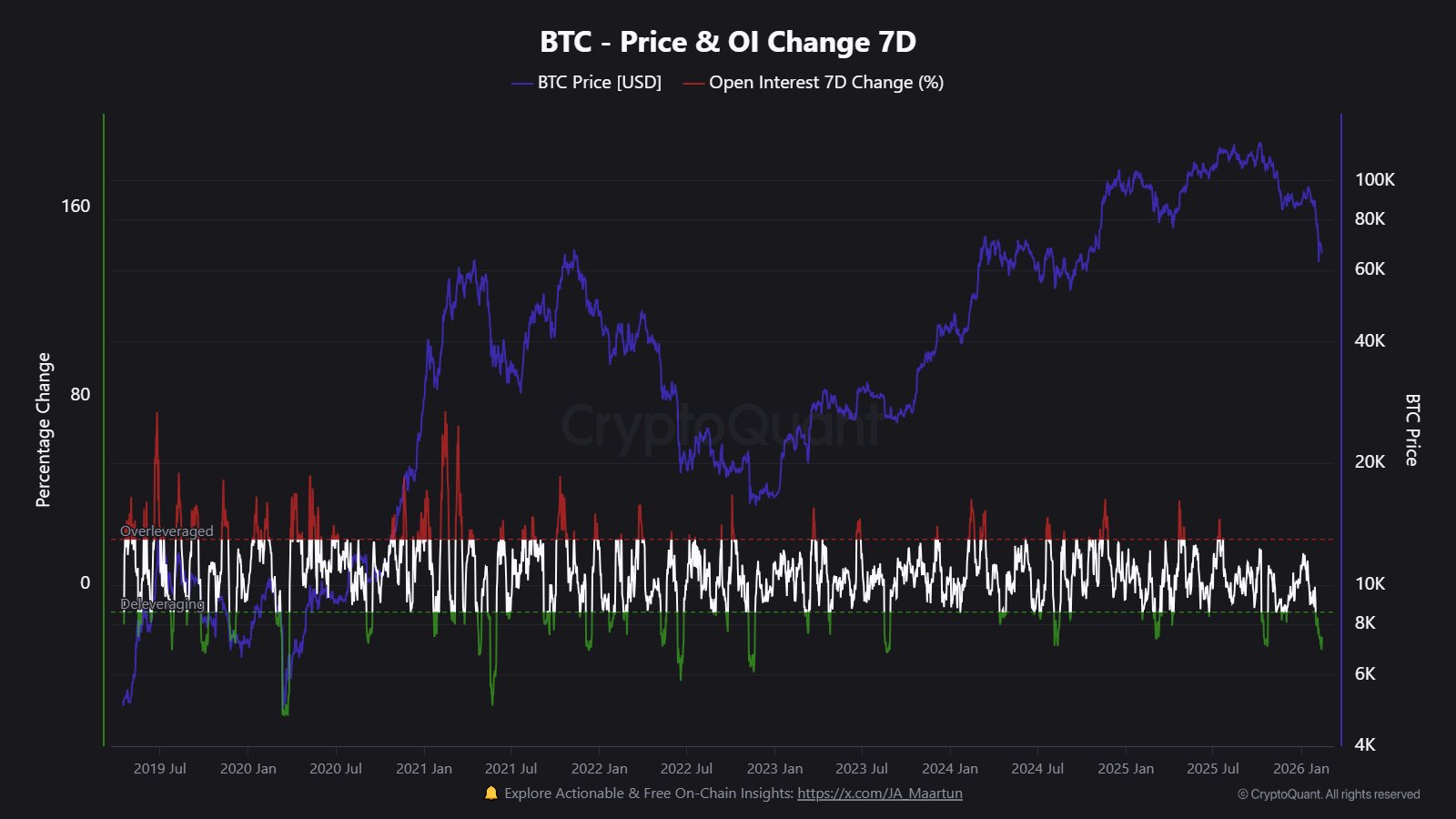

He then pairs this flow story with a mechanical reset in derivatives. Open interest has been “sliced by more than half,” falling from $45.5 billion to $21.7 billion, with a 27% drop in the last week alone. Maartunn describes this as a broad deleveraging event, painful in real time, but historically consistent with conditions that allow a bottom to form. Rather like a fellow who’s overindulged at the buffet and must now suffer the consequences, though one hopes for a swift recovery, eh?

“Look, it’s definitely painful for anyone who is overleveraged,” Maartunn remarked, “but getting rid of all that speculation is an absolutely necessary step to form a real sustainable market bottom. This is a signal of a major wash out of speculative excess.” Rather like a good spring cleaning, though one wishes it weren’t quite so brutal.

To gauge whether the drawdown is translating into capitulation-like stress, Maartunn focuses on short-term holders. He cites the short-term holder MVRV ratio at 0.72, implying the average short-term holder is down about 28%, “deep underwater” as a group. In his telling, that’s not a routine reading: it’s the lowest level since the July 2022 bottom, and a band that has historically aligned with periods of maximum financial pain. Rather like being caught in a sudden downpour without an umbrella, what?

“This level of financial stress is pretty rare historically,” Maartunn said, “and it usually happens during periods of major capitulation. Now, sure, could this ratio go even lower? Absolutely. But what history shows us is that when we get down into these levels, the risk-to-reward profile for Bitcoin starts to look a lot better.” A silver lining, if you will, though one hopes it doesn’t turn out to be fool’s gold.

Maartunn also frames the current structure as a retest of a major support cluster-where the previous cycle’s all-time high intersects the upper boundary of an older trading range-a zone that has often mattered in past cycle transitions. From there, he moves to time-based analogs, suggesting prior bear-market durations imply a broad window between June and December 2026, with the last two cycles clustering most tightly between September and November. Rather like trying to predict when the rain will finally let up, though one wishes for a bit more certainty.

His closing point is that bottoms are rarely single-day events. In his view, ETF-driven structural selling, the leverage flush, stress among short-term holders, and the retest of key levels can all coexist inside a longer bottoming process-with sentiment as the final tell.

“A real market bottom… that’s usually marked by just apathy,” he said. “When engagement on social media is totally dead, your timeline is quiet, and honestly, nobody seems to care anymore. That period of total disinterest is often the point of maximum financial opportunity.” Rather like the calm before the storm, though one hopes it’s the calm before a rather prosperous storm, what?

Overall, the implication of Maartunn’s framework is straightforward: the data may be shifting toward early bottom formation signals, but the confirming evidence, particularly around flows and sentiment, could still arrive in stages, with volatility and further stress tests along the way. Rather like a game of cricket, where one must wait patiently for the right moment to strike, eh?

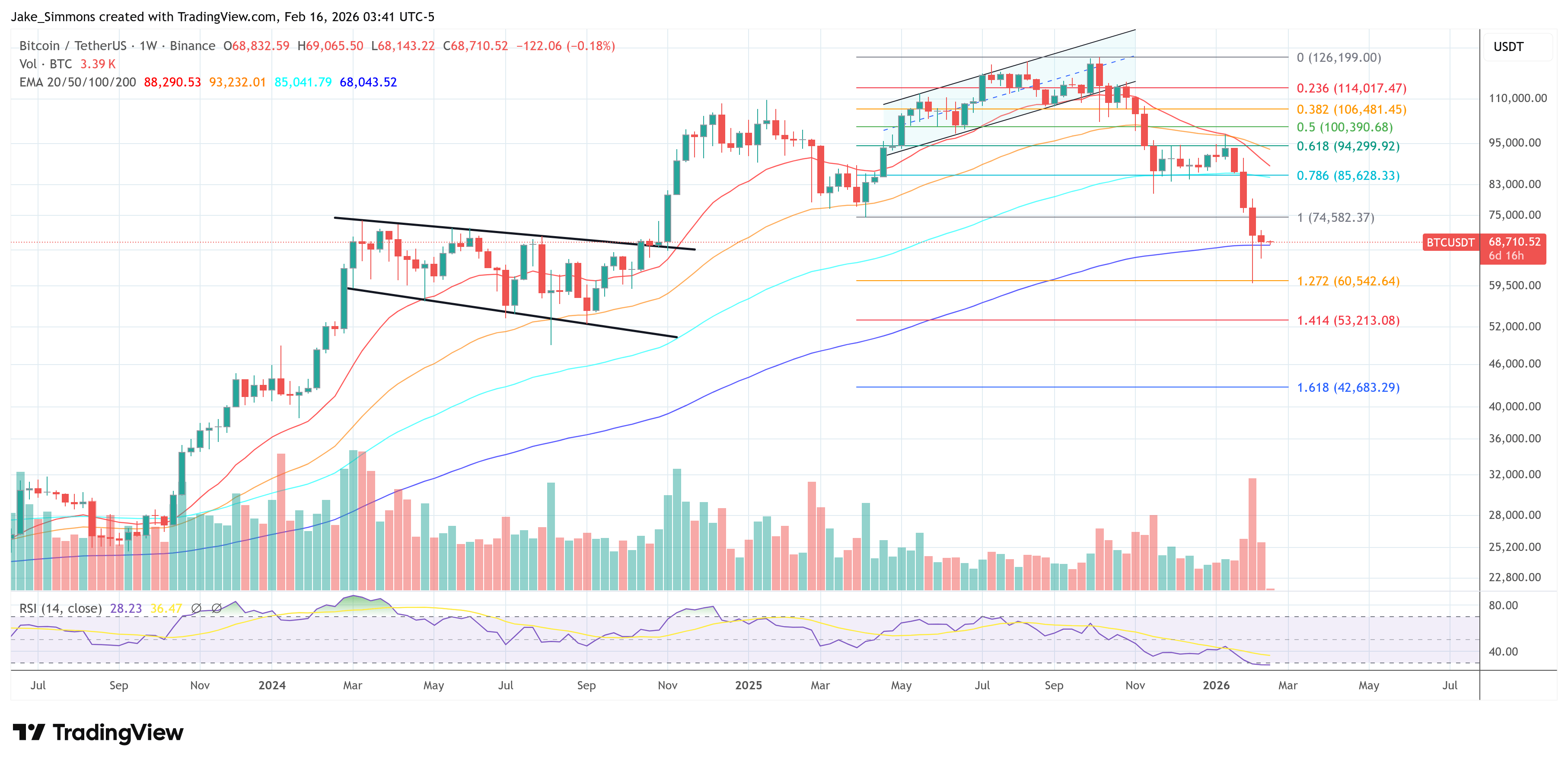

At press time, Bitcoin traded at $68,710. Not exactly a sum to be sneezed at, though one wonders if it’s the beginning of a rally or merely a brief respite from the doldrums.

Read More

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- Here Are the Best TV Shows to Stream this Weekend on Paramount+, Including ‘48 Hours’

- Top 15 Celebrities in Music Videos

- Top 20 Extremely Short Anime Series

- Where to Change Hair Color in Where Winds Meet

- 20 Films Where the Opening Credits Play Over a Single Continuous Shot

- Top gainers and losers

- 50 Serial Killer Movies That Will Keep You Up All Night

- 20 Must-See European Movies That Will Leave You Breathless

2026-02-16 12:25