Alright, settle in, you beautiful speculators! Let’s talk Datadog (DDOG 0.94%). This isn’t your grandmother’s cloud observability platform, unless your grandmother happens to be a tech wizard with a penchant for spotting undervalued assets. They alert businesses to tech glitches before customers start screaming? Brilliant! It’s like having a digital canary in a coal mine, only instead of coal, it’s the entire internet.

Now, Datadog, bless their silicon hearts, are jumping on the AI bandwagon. Not driving, mind you, more like hanging onto the back with a determined grin. They’re helping companies deploy this artificial intelligence stuff without it all crashing and burning. And guess what? People are actually paying for this! They launched a few products, and demand is… let’s just say it’s not exactly languishing. The latest earnings report? Revenue growth accelerated! I haven’t seen acceleration like that since I tried to escape a tax audit.

The stock? Down 37% from its November high. A sale! A fire sale! Don’t tell anyone, but Wall Street thinks this is an opportunity. Most analysts are saying “buy.” They’re practically throwing money at it. And those price targets? Significant. Let’s dissect this, shall we? I’ve seen more compelling evidence in a magician’s hat, but this is close.

Datadog’s AI Products: A Goldmine (Maybe)

So, they’ve got this thing called LLM Observability. It tracks costs, finds bugs, and makes sure those large language models – the brains behind all those chat bots – aren’t spewing gibberish. Essential, really. Imagine a customer service bot telling someone their order is “a slightly disgruntled aardvark.” Disaster! Then there’s OpenAI Monitoring, for those who outsource their AI brains. Smart. Like hiring a ghostwriter for your autobiography.

And they’re not stopping there! They’re prepping tools for AI agents and coding assistants. The future is coming, folks, and it’s apparently very good at writing Python. They say 5,500 customers are already using their AI stuff. That’s up 57% year over year! The Model Context Protocol server? Requests are up 11-fold! I haven’t seen numbers jump that high since I bet against a mime.

Revenue Growth: It’s Not Just Hot Air

They pulled in $3.43 billion in revenue last year. A 28% jump! And it’s accelerating. That’s like a snowball rolling downhill, only instead of snow, it’s cold, hard cash. Excluding those AI-native customers (the OpenAI types), revenue grew 29%. Those 650 AI-first companies accounted for six percentage points of the growth. Six! It’s like discovering a hidden room filled with doubloons.

Net income? $363.4 million. Up slightly. They’re spending money on research and development. Good! Investing in the future. It’s like buying lottery tickets… but with a slightly better chance of winning.

Wall Street’s Take: Are They Nuts? (Probably Not)

Forty-eight analysts cover this stock. Thirty-six say “buy.” Eight are “overweight” (bullish). Three say “hold.” And one recommends selling. One! That poor soul. Probably still using a rotary phone. The average price target? $185.92. That’s a 47% climb. But the high target? $260! Double the current price! I’ve seen more conservative predictions in a fortune cookie.

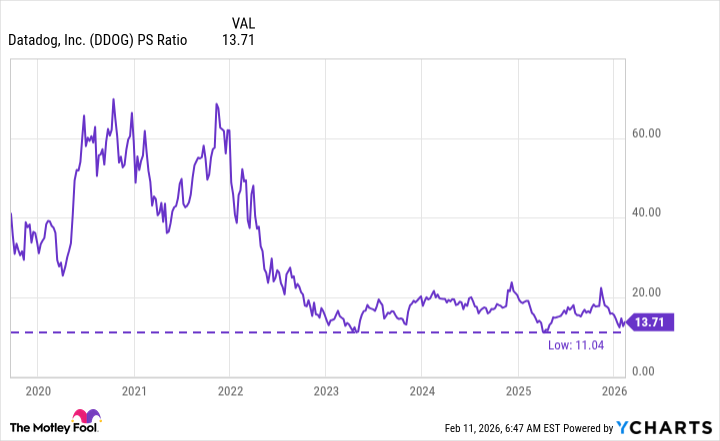

I think those targets are achievable, especially considering the price-to-sales ratio is near its lowest since they went public. It’s like finding a perfectly good suit at a flea market. They estimate their addressable market is $52 billion, and it’s growing 9% a year. They’ve barely scratched the surface! And with these new AI products, that market could get even bigger. It’s like discovering a whole new continent filled with… well, more observability opportunities.

So, yes, I think Wall Street is right to be bullish. Especially at this price. Now, if you’ll excuse me, I have a stock to buy. And a mime to avoid. Remember folks, invest responsibly… and always double-check your aardvark orders.

Read More

- 2025 Crypto Wallets: Secure, Smart, and Surprisingly Simple!

- Gold Rate Forecast

- Monster Hunter Stories 3: Twisted Reflection launches on March 13, 2026 for PS5, Xbox Series, Switch 2, and PC

- Here Are the Best TV Shows to Stream this Weekend on Paramount+, Including ‘48 Hours’

- 🚨 Kiyosaki’s Doomsday Dance: Bitcoin, Bubbles, and the End of Fake Money? 🚨

- 20 Films Where the Opening Credits Play Over a Single Continuous Shot

- ‘The Substance’ Is HBO Max’s Most-Watched Movie of the Week: Here Are the Remaining Top 10 Movies

- First Details of the ‘Avengers: Doomsday’ Teaser Leak Online

- The 10 Most Beautiful Women in the World for 2026, According to the Golden Ratio

- The 11 Elden Ring: Nightreign DLC features that would surprise and delight the biggest FromSoftware fans

2026-02-13 16:53