Dear Diary, today I found myself staring at my laptop like a confused raccoon, wondering if Warren Buffett’s $1,000 tip is a golden ticket or a trap. Turns out, the answer is: maybe. But let’s not panic. Let’s dissect this like a spreadsheet with a caffeine addiction.

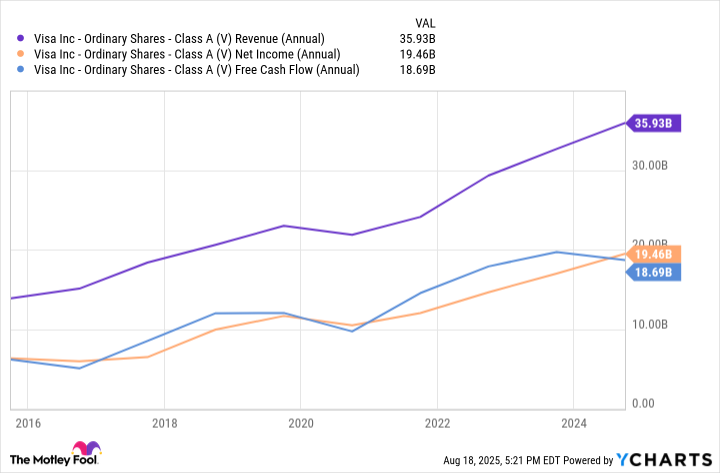

Visa’s terrific business model

So, Visa isn’t the bank that gives you a card. It’s the guy who makes sure your card works when you swipe it. Like a middleman who’s also a magician. They take a cut of every transaction, which is brilliant because it’s passive income. No credit risk, no interest rates-just a steady stream of fees. It’s like having a vending machine that never runs out of snacks. Except the snacks are digital.

But here’s the kicker: Visa doesn’t issue cards. It’s not a bank. That’s why it’s not exposed to the same risks. Imagine being the guy who owns the highway but doesn’t drive the cars. You just collect tolls. That’s Visa. And the tolls are increasing as more people go cashless. Which, honestly, is the future. Or at least, the future of my savings account.

Visa’s moat is wider than a London bridge. The more people use their cards, the more merchants want to accept them. It’s a self-perpetuating cycle. Like a dating app where everyone’s already matched. No real competition. Just a few people trying to swipe left on the idea of starting a new payment network. Spoiler: they won’t.

There is still plenty of growth left

Visa’s been around since 2008, but it’s still got legs. Digital payments are the new cash, and Visa is the guy who’s already there. Imagine if your phone could replace your wallet. That’s Visa. And even though cash is dying, it’s not dead yet. There’s a trillion-dollar graveyard of checks and cash waiting to be buried. Visa’s got a shovel.

E-commerce is the next big thing, and Visa’s already there. The US is lagging behind China and the UK in online shopping, but that’s a problem with a solution. When we finally catch up, Visa’s fees will skyrocket. Like a balloon at a birthday party. And let’s not forget: the more people use cards, the more they can’t go back. It’s a habit. Or a curse. Depending on your perspective.

Oh, and dividends. Visa’s not a rocket ship, but it’s a steady train. The yield is low, but the growth is high. It’s like a slow-burning candle-no flash, but it lasts. And if you’re the type who likes to hold on, it’s a good companion. Two shares for $1,000? That’s a bargain. Or a gamble. Depends on your definition of “bargain.”

Units of Time Spent Researching: 20 hours. Units of Panic: 5. Units of Clarity: 1. (That was when I realized I should’ve invested in Bitcoin instead.)

Anyway, Visa’s a solid pick. Not a miracle, but a methodical one. Like a well-organized sock drawer. You don’t get excited, but you don’t lose your socks either. 💵

Read More

- Spotting the Loops in Autonomous Systems

- Seeing Through the Lies: A New Approach to Detecting Image Forgeries

- Staying Ahead of the Fakes: A New Approach to Detecting AI-Generated Images

- Julia Roberts, 58, Turns Heads With Sexy Plunging Dress at the Golden Globes

- Palantir and Tesla: A Tale of Two Stocks

- Gold Rate Forecast

- The Glitch in the Machine: Spotting AI-Generated Images Beyond the Obvious

- How to rank up with Tuvalkane – Soulframe

- 20 Best TV Shows Featuring All-White Casts You Should See

- TV Shows That Race-Bent Villains and Confused Everyone

2025-08-23 10:47